Financial Assessment and Income Strategy

Before entering the retirement phase, the first step in any retirement planning checklist is a frank assessment of current assets and liabilities. For high‑net‑worth individuals, this typically includes:

- Total investable assets (brokerage accounts, 401(k)s, IRAs, Roth accounts)

- Real estate equity, including primary residence and investment properties (often overlooked in planning)

- Business interests and alternative investments (private equity, art, collectibles)

- Liabilities (mortgages, lines of credit, outstanding business debt)

- Cash and liquidity position, which will determine flexibility in retirement

The Federal Reserve’s most recent Survey of Consumer Finances shows that while median net worth rises with age, significant wealth disparities remain; even among those aged 55–64, many carry mortgage debt and lack adequate retirement savings.

With this baseline, your retirement process moves into withdrawal and income planning. This involves a diversified income pathway integrating Social Security, pensions, annuities, and investment distributions. A defined withdrawal ladder should determine sequence, timing, and tax implications of fund distributions. Stress‑testing for market downturns early in retirement mitigates sequence-of-returns risk. High‑net‑worth households often benefit from cash‑flow simulations representing decades of withdrawals under multiple market scenarios.

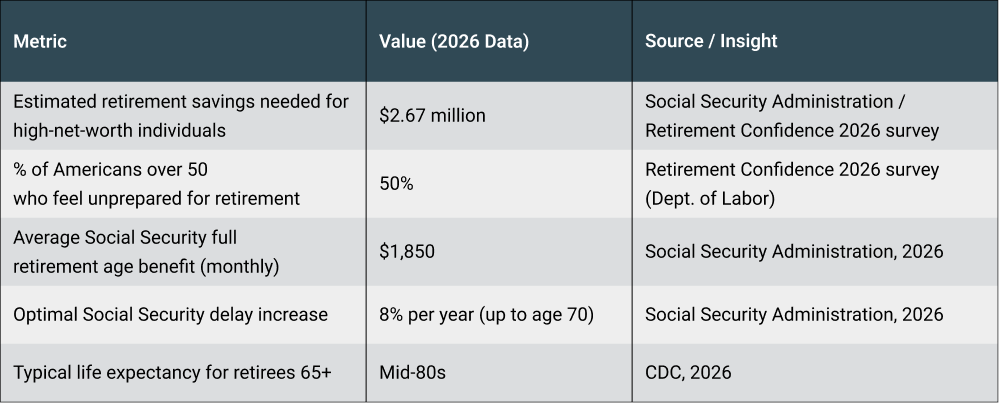

Social Security optimization is another critical lever: claiming early at age 62 reduces monthly benefits, while delaying until age 70 boosts benefits up to 8% per year. Spousal and survivor benefits, coordinated with your withdrawal strategy, further enhance tax efficiency and lifetime income.