Standard Benchmarks and Their Analytical Limitations

Professional planning standards mean going beyond the rough rules that are often shared in popular financial advice. These rules can be helpful as general guides for how to save for retirement, but they should only be treated as starting points.

The 10x–12x Salary Rule

One common rule suggests that people should aim to have between 10 and 12 times their final annual salary saved by age 67. For someone earning $150,000 per year, that means having about $1.5 million to $1.8 million saved. This rule assumes a traditional retirement age and that retirees will replace a typical portion of their working income.

The 15% Savings Guideline

To reach those long‑term retirement goals, many experts suggest a how-much-to-retire guideline of about 15% of your pre‑tax income each year. This percentage usually includes both your own savings and any employer match from retirement plans. When considering “how much should I have on my 401k?”, remember that early momentum is frequently aided by automatic enrollment in these plans.

The Rule of 25

The “Rule of 25” works from the idea of withdrawing about 4% per year in retirement. To estimate your target savings, you multiply your desired annual withdrawal by 25. For example, someone who wants $80,000 per year from investments would need roughly a $2 million portfolio.

Critical Analysis: Data over Guesswork

While these rules are helpful for quick estimates, they ignore many important details. They usually do not account for taxes, market timing risk, or unexpected health costs. Because of this, relying only on general rules can create unpleasant surprises.

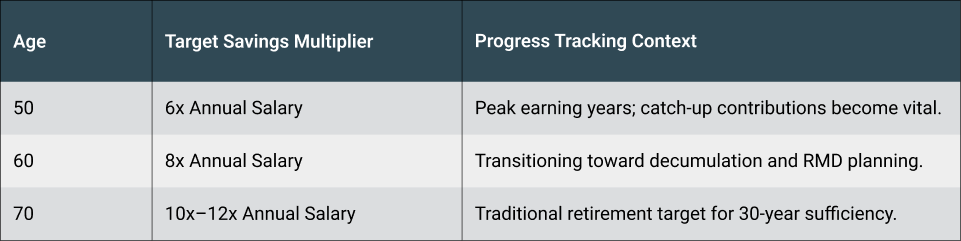

For example, the Rule of 25 assumes a retirement lasting about 30 years. Someone asking “how much do I need to retire at 55?” could easily need a larger multiplier, such as 33 times their annual spending, to make sure the portfolio lasts longer. Those researching how to retire at 50 or, indeed, how much to retire at 60, must also account for these extended time horizons.

A good retirement advisor will prefer to use detailed financial models rather than guesswork. This allows them to test how a portfolio might perform under different economic conditions.