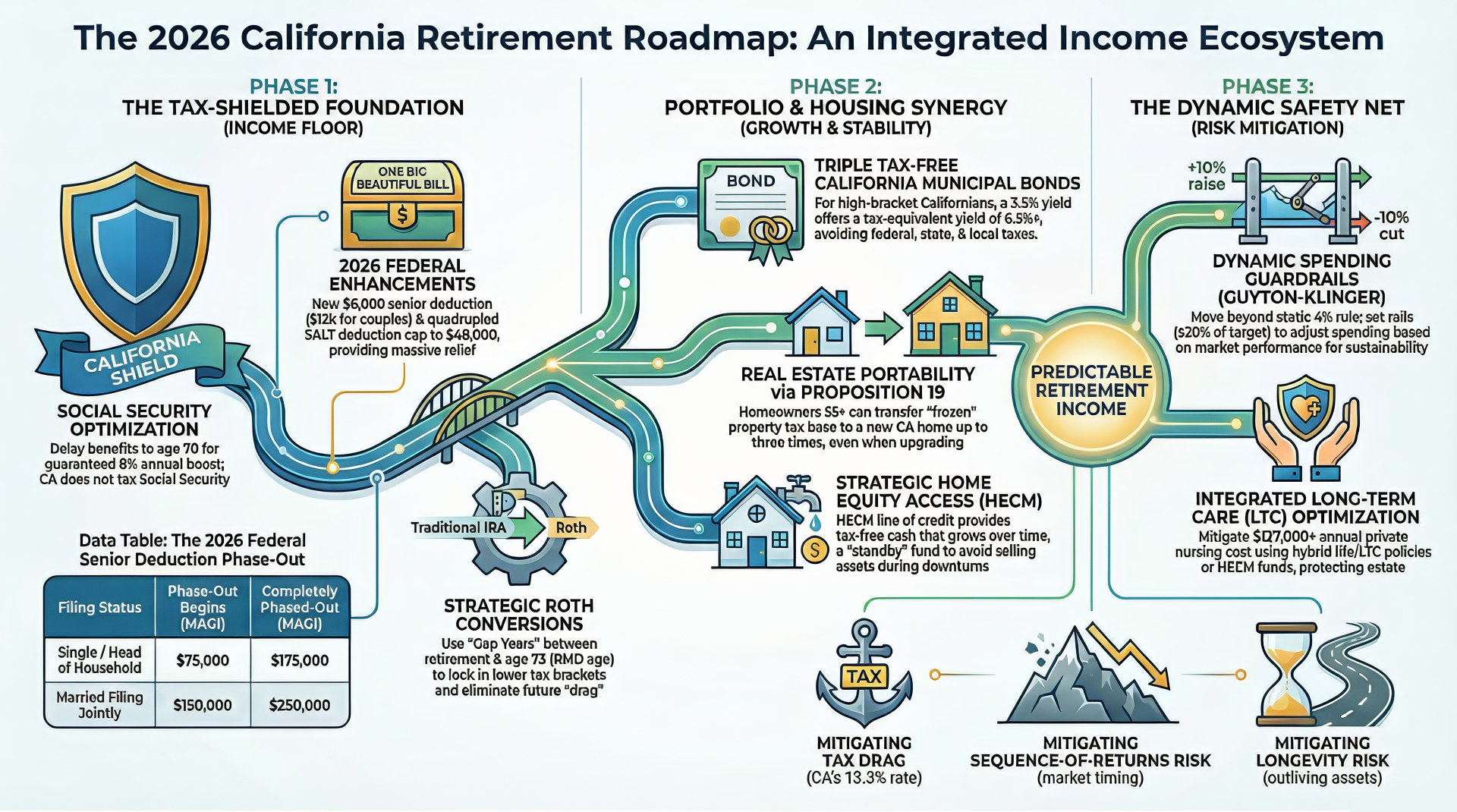

Leveraging Local Tax Shields and High-Yield Fixed Income

1. Delay Social Security and Use the California Shield

California doesn’t tax Social Security, while the federal government can tax up to 85%. For a typical retired couple, this can protect nearly $1 million from state taxes over 20 years. Waiting until age 70 to claim your benefits can increase your guaranteed income by about 8% per year, giving you more tax-free money and peace of mind for the long run.

2. Invest in Triple Tax-Free California Municipal Bonds

Some California municipal bonds are tax-free at the federal, state, and local level. For high earners, that’s a huge win compared with taxable bonds. A bond paying 3.5% tax-free can work like it’s paying over 6% in a regular account—so your money stretches further every year.