Roth IRAs: A Tool to Maximize Tax Efficiency or Start Your Family on Their Way Toward a Healthier Retirement

- 18

- Jun

Paying taxes is so ingrained in our lives that many people do not even think about tax reduction until it’s time to file their tax returns. Unfortunately, by that point it’s usually too late to implement a strategy for minimizing their tax bill.

Paying taxes is so ingrained in our lives that many people do not even think about tax reduction until it’s time to file their tax returns. Unfortunately, by that point it’s usually too late to implement a strategy for minimizing their tax bill.

It’s extremely important that you take your tax efficiency into your own hands. The concept of “let’s deal with taxes when the time comes,” many times is usually not the best plan. One of the biggest tax benefits available to most investors is the ability to defer taxes offered by retirement savings accounts, such as 401(k)s, 403(b)s and IRAs. Through the use of tax deferrals, investors have the opportunity to grow their wealth faster.

Traditional retirement accounts can offer a potential double dose of tax advantages. For those who qualify, contributions made may reduce current taxable income (when income eligibility requirements are met) and any investment growth is tax-deferred. After age 70½, however, there are required minimum distributions (RMDs) that you must take. Also, upon death, your beneficiaries will be required to pay taxes.

Roth IRAs are different. With a Roth IRA (if income eligibility requirements are met) you can only contribute after-tax dollars. A Roth IRA contribution won’t reduce your taxable income the year you make it, however, there are no taxes on your future earnings and no penalties when you take a distribution, provided you hold the account for 5 years and meet one of the following conditions: you are age 59½ or older; are disabled; make a qualified first-time home purchase (lifetime limit $10,000); or have died. Also, be aware that while your earnings may be subject to taxes and penalties if withdrawn before those conditions are met, your contributions can be withdrawn at any time without tax or penalty. Roth IRAs have no required minimum distributions (RMDs) during the lifetime of the original owner so they can also be useful vehicles for estate planning.

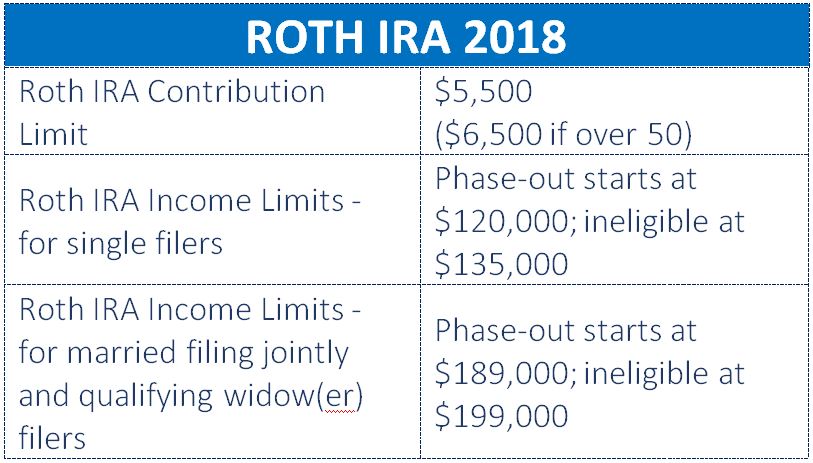

Most experts agree that consistent funding of a retirement plan is a healthy activity. The chart in this article shows the 2018 IRS income limits for those who contribute to Roth IRAs.

Considering Roth IRA Conversions

Prior to 2010, to be able to convert from a traditional IRA to a Roth IRA, your income needed to be under a certain limit. The IRS rules have changed and there is no longer an income cap for Roth IRA conversions. With the cap removed, regardless of your income, anyone can now convert to a Roth IRA, as long as they pay the appropriate tax on the conversion. If you convert to a Roth IRA, you will have to pay taxes on any tax-deferred deposits and investment gains at the time of the conversion.

Why Convert to a Roth IRA?

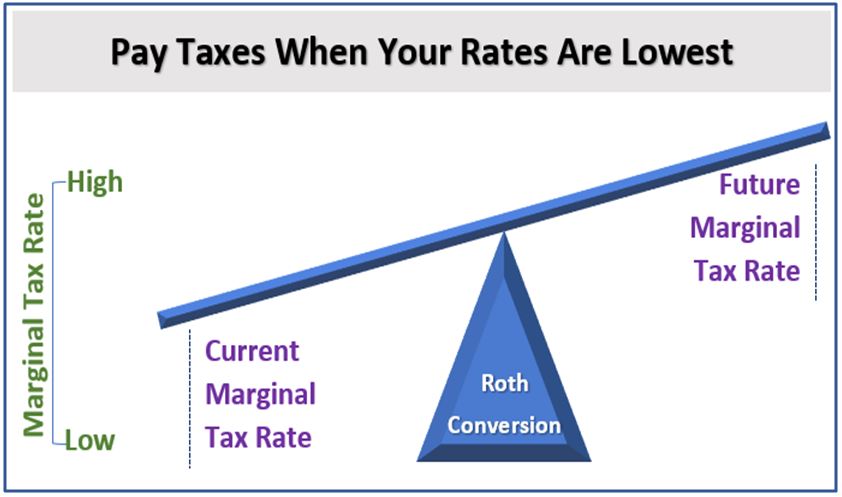

Tax-savvy investors want to pay as little income tax as possible. Converting to a Roth IRA may allow you to make a tax move that will save you or your beneficiaries money in the long run.

For example, if you anticipate your income dropping significantly in a certain year (and increasing in following years), you could plan a conversion (or partial conversion) for the low-income year. Since your income is lower, you may be in a lower tax bracket when you convert.

Similarly, if the government announces a tax-rate increase to go into effect in a future year, a conversion in the current year could possibly save income tax.

Converting to a Roth IRA could assure that you will owe no additional income tax on the converted funds—and any money those funds will potentially earn before you withdraw them—during retirement. The balance in your portfolio likely will be what you can take out and use in retirement and you most likely won’t have to calculate an after-tax balance.

Partial Roth IRA Conversions

Making a Roth IRA conversion does not have to be an all or nothing decision. Although the rules surrounding partial conversions can be complex, a competent financial professional can help you understand the tax impacts and rules that govern converting some, all, or none of your existing IRA to a Roth IRA. Like any other decision, all of the variables of your particular situation should be considered. You should consider running the numbers for your situation to best determine the impact of making a full or partial conversion to a Roth IRA.

For example, suppose you are a married taxpayer filing jointly with $50,000 of taxable income and you have $300,000 in a traditional Roth IRA. Your marginal tax bracket is 12%. However, if your income increases above $77,400 you move into the 22% bracket. You might wish to convert up to $27,400 of your traditional IRA to a Roth IRA. From a taxwise perspective this could be more attractive than a full conversion, because if you converted the entire IRA this year, you could pay tax on some of the conversion at rates as high as 32%.

Roth Conversions in Low Tax Years Could Be Attractive

A good time to explore a partial Roth conversion can be during a year when you have a lower income than you expect to have in the future. This could include someone who just retired, is no longer employed, or has made large deductible charitable gifts.

Partial Roth conversions typically make the most sense in low income years. They can be helpful when you are in the early years of retirement (before RMDs & Social Security begin). In this instance, you can consider converting some of your IRA assets to a Roth IRA and paying federal ordinary income taxes (and state taxes where necessary) on the amount converted.

If you do not use Roth IRA conversions when you are in low tax brackets during low income years, you will be forced to take out minimum required distributions (RMDs) from your traditional IRA funds at age 70½,  when you might be in a higher tax bracket, thus increasing the amount of taxes you pay during that time. A pre-70½ year old can take advantage of any low tax years if their marginal tax brackets will likely be increasing because required minimum distributions (RMDs) and Social Security might move them to a higher tax bracket in the future.

when you might be in a higher tax bracket, thus increasing the amount of taxes you pay during that time. A pre-70½ year old can take advantage of any low tax years if their marginal tax brackets will likely be increasing because required minimum distributions (RMDs) and Social Security might move them to a higher tax bracket in the future.

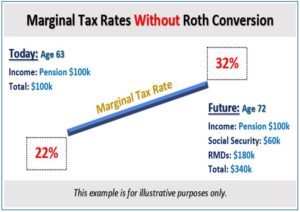

As an example, let’s look at a 63-year old in a married household who files a joint tax return and also has a significantly large traditional IRA. The traditional IRA will begin requiring RMDs at age 70½ and Social Security payouts must begin by age 70 as well. If this household’s only source of income is $100K from a pension, this year, they might pay a marginal tax rate of 22%.

In nine years, when the main IRA holder is now 72, the pre-tax IRAs will have had a lot of time to potentially grow. This household could expect to have significant required minimum distributions (RMDs) and Social Security income on top of the $100k pension. If the RMD’s at age 72 are about $180,000 and the household Social Security is $60,000, then this household which only had $100,000 of income at age 62 now has $340,000 of income. This could increase their marginal tax rate by 10% to a total of 32%.

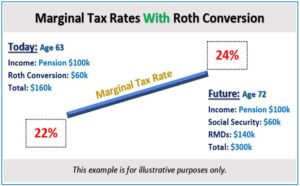

On the other hand, if this household were to employ a partial Roth Conversion, it would allow them to pull future income forward taking it out at a 22% rate instead of a 32% marginal rate! By taking an additional $60,000 of income each year for the next nine years, through the converting of $60,000 IRA money to Roth IRA money, they will be required to pay taxes. These strategic conversions will become Roth IRA assets and decrease the size of the traditional IRAs. This lowers future RMDs and with all things equal, it could decrease their total future income and shift their future marginal tax bracket to a lower rate of 24%.

Who Is in a Higher Tax Bracket?

It is generally more advantageous for a decedent to leave assets that do not have an attached income tax liability. Traditional IRAs have embedded tax liabilities. If you or your living parents have assets in a traditional IRA and are planning on leaving them someday to a beneficiary who is in a higher tax bracket, then it might be in your best interest tax wise to consider reviewing a schedule for a partial or full Roth IRA conversion strategy.

A Roth IRA conversion essentially changes an asset with an embedded income tax liability to one with no such tax liability. As a result, a Roth IRA conversion may minimize, or even help avoid, the double taxation if there is a taxable estate. Regardless of whether an IRA owner expects to leave a taxable estate, “pre-paying” the income tax may be attractive in several instances. These can include:

- When the IRA owner’s income tax bracket is lower than, or the same as the beneficiary’s tax bracket.

- When the IRA owner has a taxable estate and can afford to pay the taxes with funds outside the IRA.

- When there is a long-term time horizon. (Note: converting typically requires a 5-year hold period to avoid penalties and the result is more tax advantageous.)

To discuss your overall retirement distribution strategy call us and schedule an appointment.

To discuss your overall retirement distribution strategy call us and schedule an appointment.

Roth IRAs and Your Children (or Grandchildren)

Many people think they can hold off saving for retirement when they are younger and make up the difference later. Savvy investors know this can be a costly mistake. Waiting too long to start saving can make it very difficult to catch up and only a few years can make a big difference in how much you’ll accumulate. For some, having a large retirement account might seem like a nice but unattainable goal. It can become more realistic if they know the secret: time. When should you start saving for retirement? It might seem backwards to worry about the last money you’ll need early in life, but because compounding over time can be so powerful, starting early gives you more flexibility later on in life. If you have children (or grandchildren) who earn money, now might be a good time to help them start or fund a retirement account. While they can always fund a traditional IRA, if they qualify, a Roth IRA might be an even better choice.

Custodial Roth IRAs

Starting retirement savings early can allow you the potential advantage of growing money in a tax efficient account over a long period of time. Many children work before they reach age 18. The income they earn makes them eligible to contribute to a Roth IRA, which can be an extremely smart move for teenagers. This can also provide an excellent opportunity for you to teach or reinforce with your children the importance of saving money.

Historically, some financial institutions did not let minor children open a Roth IRA. Fortunately, some institutions will let parents act as a custodian on a Custodial Roth IRA for the benefit of their children. Some of the rules regarding Custodial Roth IRAs are:

- In order to be eligible to open a Custodial Roth IRA, the child must meet all the same requirements as an adult would. The minor must have earned income and contributions are limited to the lesser of total earned income for the year and the current maximum set by law, which for 2018 is $5,500.

- Also, adjusted gross income for the child must be below the thresholds above which Roth IRAs aren’t allowed.

- Even though the custodian is the legal owner of the account, the Roth IRA must be managed for the benefit of the minor child.

- As the custodian, you make the decisions on investment choices—as well as decisions on if, why, and when the money might be withdrawn—until your child reaches “adulthood,” defined by age (usually between 18 and 21, depending on your state of residence). Once they reach that age, the account will then need to be re-registered in their name and it becomes an ordinary Roth IRA.

If you’re the parent of a child who has earned income, a Custodial IRA can be a great way to teach the value of saving and investing. Besides getting a head start on saving, your child may be able to use the funds for college expenses—or even to buy a first home.

There are several ways to make a Custodial Roth happen. For example, you can potentially use your annual ability to gift to children or grandchildren to make this happen. If your child or grandchild is earning money, call us and we can discuss your options for setting up Custodial Roth IRAs.

Please share this information with others!

This year, our goal is to offer services to several other clients just like you! If you would like to share this information with a friend or colleague, please call Financial Advisors Network, Inc. at (714) 597-6510 and we would be happy to assist you.

Conclusion

Saving for retirement has and always will be a priority for most investors. Should you convert to a Roth IRA? If so, how much and when? These are good questions that require an examination of your personal situation and goals. This is an area where a highly informed financial advisor can help you make an educated and calculated decision. We realize the decision to convert some or all of your retirement account to a Roth IRA is complex. A Roth IRA can be a very good planning tool. Among its many advantages, Roth IRAs allow your money to grow tax free and withdrawals are tax free as well. Please note that although Roth IRAs can be attractive tax wise, Roth IRAs have rules and limitations. While this article is for informational purposes only and should not be deemed tax advice or an individualized recommendation, we hope that some of these points are helpful to you.

We welcome the opportunity to help you map out a strategy that will be best for your situation. To discuss your personal situation call us and schedule an appointment.