Q4 Newsletter

- 16

- Jan

2023 is in the books and the last quarter left investors looking forward to a bright and happy new year. Historically, equities typically have advanced in the fourth quarter, and we can now add 2023 to that statistic.

We entered the fourth quarter with strong momentum, including a healthy labor market and easing inflation pressures. We then ended the quarter with a record high for the Dow Jones Industrial Average (DJIA), as it closed over 37,000 for the first time. The S&P 500 ended the year with a gain of more than 24% and the Dow Jones Industrial Average (DJIA) ended the year up more than 13% (cnbcnews.com; 12/29/23).

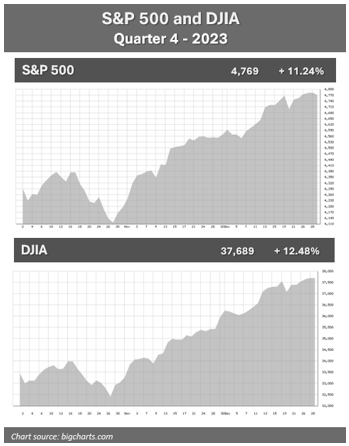

The S&P 500 was up nine weeks straight in the fourth quarter. The S&P 500 was four points away from its all-time high of 4,797 on December 28, but then pulled back and closed the quarter at 4,769. The Dow Jones Industrial Average (DJIA) reached an all-time high and ended the quarter at 37,689 (Barrons; 1/1/2024).

This jump was primarily a result of the Federal Reserve signaling a pivot from its aggressive monetary position and indicating that interest rates would be cut several times in 2024. The Federal Reserve left interest rates untouched in the fourth quarter due to the continued slowdown of inflation.

“Inflation has eased from its highs, and this has come without a significant increase in unemployment. That’s very good news,” stated Fed Chair Jerome Powell during a news conference following the December FOMC meeting. Fed officials see core inflation finishing 2023 at 3.2%, and 2.4% in 2024, then to 2.2% in 2025, resting at its final destination of 2% in 2026 (cnbc.com, 12/12/23).

Throughout the year, the labor market has been slowly cooling down. The thriving labor market and wage growth are key indicators tracked by the Federal Reserve to help determine how they will move interest rates. The unemployment rate was reported at 3.7% in November.

The last quarter of 2023 could have been a pivoting point for equities. Over the past few years, the primary focus for investors has been inflation and interest rates, and many hunkered down with a focus on retention, not gains. If interest rates begin to stabilize, this could help support higher stock valuations and provide potential reentry points in 2024. A soft landing might come to fruition in the coming year. Inflation stabilizing or becoming stagnant, lower interest rates, a strong labor market, and confident consumer spending are all positive news. These are some of the items investors can be grateful for. However, with optimism abounding and investors potentially beginning to come out of the shadows, this is not the time to throw caution to the wind. 2024 brings a presidential election, geopolitical unrest continues, and pandemic-era savings are dwindling.

As financial professionals, we are committed to keeping our clients apprised of any changes and activity that could directly affect their unique situation. While 2023 rewarded our focus of being disciplined with long-term equity investments, we enter 2024 with our continued mantra of “proceed with caution.” Now is a good time to review your investments and confirm they are still congruent with your time horizon, risk tolerance, and goals.

Inflation & Interest Rates

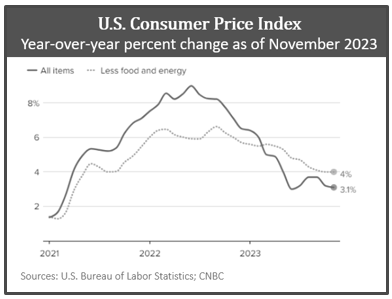

Inflation pressure continued to ease in the fourth quarter. In October, the 12-month percent change in all items in the Consumer Price Index (CPI) decreased to 3.2%, following gains of approximately 3.7% in August and September. In November, the slowing trend continued, clocking in at a 3.1% increase compared to a year earlier. While we have seen a significant improvement from the 9.1% peak in June of 2022, there is still a way to go to reach the Federal Reserve’s target of 2%.

The November core CPI (which excludes food and energy prices), which is used by many economists as a better indicator of future inflation, was up 4% from the year prior. While this is not the best of news, it is still well below its recent historical peak of 6.6% in September.

At their December Fed meeting, the central bank lowered its inflation forecast for 2024 from 2.6% to 2.4%. Overall, we are still seeing a trend in the right direction.

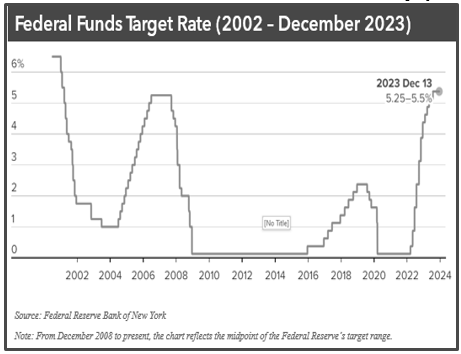

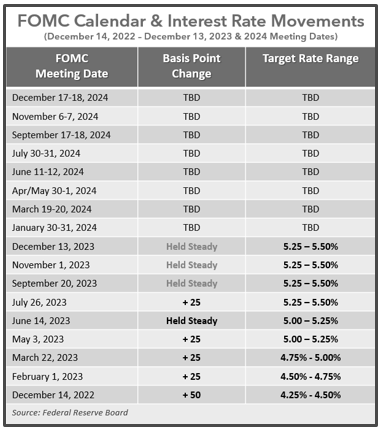

As a result of inflation easing and the economy maintaining its strength, the Federal Reserve held rates steady at their final meeting of 2023. This is the third straight time the FOMC has not raised rates, and the target rate range remained at 5.25-5.5%.

The Fed had raised interest rates a whopping eleven times since March of 2022, thus this three-time consistency of rate stagnancy was well

received by investors. Even better news was that the minutes shared that the Feds suggested rate cuts in 2024.

In the Federal Reserve’s official press release after the December meeting, it stated, “Recent indicators suggest that growth of economic activity has slowed from its strong pace in the third quarter. Job gains have moderated since earlier in the year but remain strong, and the unemployment rate has remained low. Inflation has eased over the past year but remains elevated. The U.S. banking system is sound and resilient. Tighter financial and credit conditions for households and businesses are likely to weigh on economic activity, hiring, and inflation. The extent of these effects remains uncertain. The Committee remains highly attentive to inflation risks.”

It confirmed that the Fed will continue to fervently pursue its inflation rate goal of 2% and will, “adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee’s goals. The Committee’s assessment will consider a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments” (federalreserve.gov, 12/13/23).

Equity markets responded very favorably to this news and the DJIA jumped more than 500 points, passing the 37,000 threshold for the first time (www.cnbc.com, 12/13/23).

Interest rates and inflation are integral to financial planning so we will continue to keep a close eye on their movements. While the efforts of the Fed’s stringent monetary tightening policies the last few years are now being seen, the Fed still maintains its willingness to raise rates again should inflation reverse direction. Although we cannot predict what the Fed’s next move will be, we will continue to follow key economic indicators for our clients.

The Bond Market & Treasury Yields

Thanks to a year-end surge, bond prices had a historic rally and after two straight years of losses, bond investors saw a positive year-end. Bonds were still in the negative until mid-November, and the closing rally in the fourth quarter ended their two-year losing streak.

Deutsche Bank Research’s Jim Reid stated, “It was a positive year for most financial assets, but in several cases, the gains were almost entirely driven by the final two months.” He continued, “If we’d have stopped in late-October, then bonds would still have been on track for a third consecutive annual loss” ( marketwatch.com; 1/2/2023).

2023 was a significant year for treasury yields. In October, the 10-year treasury yield reached 5%, the first time in 16 years, before tempering back down. On December 29, the 10-year note was 3.88%, as compared to the end of the third quarter, where it reached 4.59%. The 20-year treasury ended the fourth quarter at 4.20% and the 30-year note closed at 4.03% (treasury.gov).

The sudden pivot in bonds is testament to the volatility we have seen in 2023. It also reminds us how much weight Fed movements carry. We will continue to closely monitor how the Fed’s movements and how rising interest rates are affecting bond yields. With the Feds anticipating interest rate cuts in 2024, this may narrow the opportunity to get lower-risk, higher-yielding bonds.

For anyone who is interested in exploring adding more bonds as part of a diversified portfolio, please contact us. As your wealth manager, we want to help you make the best decision for your portfolio. Please remember, while diversification in your portfolio can help you pursue your goals, it does not ensure a profit or guarantee against loss.

Investor’s Outlook

The end of the fourth quarter brought investors into the new year with optimism and anticipation. Looking forward to 2024, investors are hopeful and are beginning to see the light at the end of the pandemic-induced tunnel. Recession fears have significantly diminished, and a “soft-landing” or a shallow recession appears to be more possible.

It is believed that real GDP growth will regress but remain healthy and the labor market will remain strong. It’s also anticipated that inflation will continue to lose steam and will decline to about 2.5% in 2024 (stlouisfed.org,11/28/23).

The interest rate hiking cycle currently seems to be coming to an end and many economists anticipate seeing the 5.25–5.5% rate as a high point until the Fed potentially commences with an interest rate cut cycle.

This can be good news for the investor, and overall, 2023 was a healthy year. The biggest question now is – will this rally continue into the new year?

Some things to keep an eye on in the coming months include energy and housing costs. There was good news at the gas pump, as gas prices were down 8.9% over the past year.

Although not in the core Consumer Price Index, declining gas prices can be a key player in consumer sentiment and spending habits. Since consumer sentiment is rebounding, gas prices have begun to decline. This is strongly welcomed at the gas pump. The national average for unleaded was $3.14 on December 12, the lowest all year, according to AAA. One month prior, it was $3.37. Higher prices, such as in California, drove this average higher, however, in many states, consumers could readily find unleaded gas for under $3.00. The decline in gas prices has been a key player in the slowdown of inflation (nytimes.com, 2/12/23).

Shelter costs are still historically high, but on a slow downtrend. For now, housing costs remain persistent, up 6.5% year-over-year in November. In the coming year, purchasing a house may be in closer reach for some home buyers. In October, the average 30-year fixed-rate mortgage hit its 2023 high. During the remaining fourth quarter, it receded by over half a percent (nytimes.com 12/11/23).

While things are looking up, throwing a good riddance party to market volatility may be premature. The coming year could still bring instability and uncertainty. Economic growth could decelerate in 2024.

Could an economic slowdown ruin the party – and the stock market? Geopolitical strain on the economy is still a major concern with the ongoing Russia-Ukraine war, conflict in the Middle East, and continued tensions with China.

The U.S. also have a presidential election, which can be one of the major influencers of the market movements in 2024. A new cabinet could signal major changes to the economy and tax law.

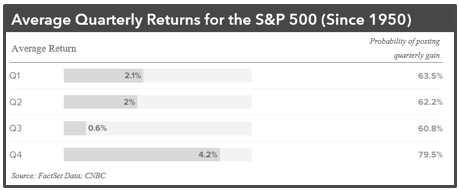

Since 1952, the average gain in the S&P 500 during a presidential election year is 7%. During a re-election year, the average annual gain is 12.2%. The average is 10% annual total returns for this major index in a non-election year. However, please remember that past performance does not guarantee future returns. (money.usnews.com, 12/11/23).

Fed officials will be keeping a close eye on key indicators such as housing, labor markets, and core goods that will help them when determining monetary policy. While the Fed anticipates rate cuts in 2024, as the last few years have reminded us, it is best to be prepared for the unexpected.

2023 rewarded long-term investors and regardless of what 2024 will bring, it is always prudent to watch your expenses and make smart money and investment decisions. We believe in proactive preparation and our goal is to provide you with a solid financial strategy that is carefully designed to withstand any market environment. From an investor standpoint, we stand by our belief that investing in equities is a long-term commitment. Heading into a new year, which is also the election year for one of the most raucous races we have seen in recent history, we believe that volatility could still be prevalent and that investors should be cautious in any financial decisions. A long-term strategy needs to be a benchmark for smart investors.

While we are not in the business of trying to predict the future, Wall Street’s top strategists have released their forecast for the year ahead, with the average consensus that the S&P 500 will climb by about 10%, the historical average in this major index (finance.yahoo.com; 12/3/23).

Heading into the new year, we will continue to keep an eye on inflation rates, economic growth data, and monetary policy moves. The coming months bring much uncertainty, and you should not let the recent market surge deflect you from your long-term strategy and goals. The media will be buzzing with daunting, speculative claims and predictions, and confusing information with the upcoming election. We recommend you minimize your viewing of news and social media.

We suggest periodically rebalancing your portfolio to confirm that your risk tolerance, time horizon, and asset allocations are all still in alignment with your goals. Now is a great time to consider this healthy practice. Also, if you haven’t already done so, review your annual budget for 2024 and make any modifications to assist you with any anticipated needs throughout the year.

A few reminders:

- You can still contribute to IRAs for the tax year 2023. The deadline to contribute is April 15, 2024.

- This is a good time to recheck your estate plan (including your beneficiaries).

- Please notify us of any items or changes that you anticipate this year, such as retiring, adjustments to your estate plan, or important tax “birthdays.”

- If you would like to, review your financial situation directly with us.

Our goal in 2024 is to exceed our client’s expectations. We take pride in offering service that includes:

- A proactive, individually tailored approach to our client’s financial goals and needs.

- Consistent and meaningful communication throughout the year.

- A schedule of regular client meetings.

- Continuing education for all our team members on issues that may affect our clients.

- Proactive planning to navigate the changing environment.

We always recommend discussing any changes, concerns, or ideas that you may have with us prior to making any financial decisions so we can help you determine the best strategy. There are often other factors to consider, including tax ramifications, increased risk, and time horizon changes when altering anything in your financial plan.

Please remember that as a valued client, we are accessible to you. Feel free to contact us with any concerns or questions you may have. We appreciate the trust and confidence you place in our firm and look forward to serving you in 2024 and beyond.

What’s for dinner?

Deciding whether to eat or dine out?

This may help you answer the age-old question…

According to the United States Department of Agriculture (USDA), in 2023, food-at-home prices are predicted to have increased about 5%. Food-away-from-home prices are predicted to have increased approximately 7.1%.

In 2024, all food prices are expected to rise even more, with an overall increase of 1.2%, with food-at-home prices predicted to decrease 0.6%. However, if you’re planning on eating out, expect to pay an additional 4.9% (USDA Economic Research Summary Findings. Food Price Outlook, 2023 and 2024).

We want to offer our services to other people just like you!

Many of our best relationships have come from client introductions. Do you know someone who could benefit from our newsletters and articles? LEt us know and we can add them to our mailings.

We would be honored if you would:

- Add a name to our mailing list

- Encourage someone to schedule a complimentary financial consultation

Please call us at (714) 597-6510 or email info@fanwmg.com. We would be happy to assist you!

Upcoming Events

- Tax Planning Webinar | Wed, Jan 17 at 6 pm

- Retirement Classes | Jan -Feb on Wed, Thu, or Sat at IVC

- Investments Webinar | Wed, Feb 21 at 6pm

- Property Inheritance Webinar | Wed, Feb 28 at 6pm

- Social Security & Medicare Webinar | Wed, Mar 6 at 6pm