Proactive Planning for Upcoming Sunset of State Tax Law Changes

- 12

- Mar

Communication and planning have always been essential when attempting to transfer wealth efficiently. Tax planning can also play a significant role for larger estates. Currently, the federal estate tax laws are very generous, however, when the 2017 Tax Cuts and Jobs Act (TCJA) rules expire at the end of 2025, that might not be the case. We believe in proactive tax planning and waiting until the tail-end of these time-constrained rules could cost you. We like to be ahead of changes, especially when it comes to potentially major tax liability.

The Tax Cuts & Jobs Act (TCJA)

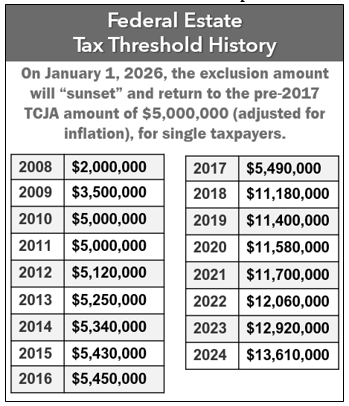

Starting in 2018, the TCJA doubled the estate and gift, and GST tax exclusion amount. As our chart shows, this exclusion has moved from $5.49 million for an individual in 2017, all the way up to $13.61 million in 2024. For couples in 2024, the tax exclusion is $27.22 million.

The doubled amount sunsets, or expires, on December 31, 2025. For high-net-worth individuals, this could affect wealth transfer strategies. As the tax law presently stands, the current lifetime estate and gift tax exemption will revert to pre-TCJA levels and will be cut in half and adjusted for inflation on January 1, 2026. With current inflation statistics, this could bring the amounts to around $7 million for individuals and $14 million for couples in 2026.

While there could very well be new tax legislation between now and the expiration date, when reviewing estate plans, families should consider that this TCJA provision is scheduled to expire. Proactive estate and tax planning could help avoid a costly missed opportunity.

While many Americans do not need to worry about this sunsetting tax law, as their net worth does not meet the minimum, it is still important that they have estate planning documents to help transfer assets and wealth to their loved ones efficiently. Also, some states have estate tax transfer taxes that start at much lower levels than the federal amount. Those who are close to the potential after sunset federal limits, but not there yet, should watch the growth of their net worth to stay on top of it. Wealthy individuals and families should not procrastinate, and we recommend planning now to ensure preparedness for the pending drastically reduced limits.

In this article we want to provide you with valuable information. However, navigating estate planning can be challenging and difficult, so checking with both your estate planning professional and financial professional is always advised. We are always available if you have any questions regarding your personal financial situation.

Wealth Transfer & Strategic Gifting

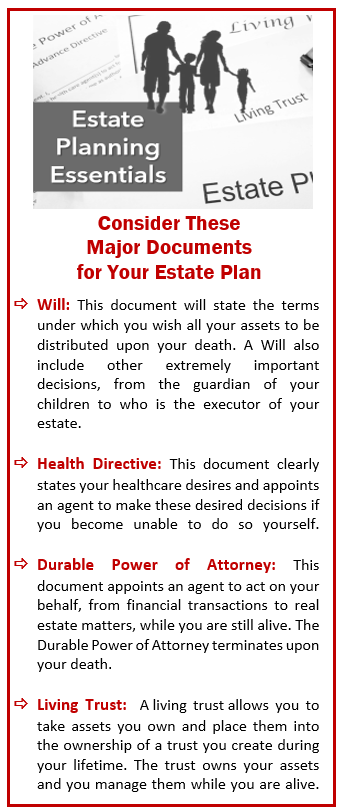

The passing of a loved one brings many emotional challenges, so having your estate plan carefully prepared well in advance can offer the solace of knowing your loved ones will not have to navigate financial and legal challenges while they are grieving. There are two major ways to transfer wealth: leaving an inheritance after you pass, or gifting during your lifetime.

The latter can be particularly alluring and can offer some tax-saving possibilities. Many families can look at transferring wealth during someone’s lifetime without incurring any federal gift or estate taxes. This is usually in addition to the annual exclusion for gifts, which in 2024 is $18,000 for individuals and $36,000 for couples.

For example, John has an estate valued at $15 million and in 2024 transfers $10 million to a trust for his children. Under the current TCJA provisions, he can use the $13.61 million exclusion to make that $10 million transfer tax-free. However, if he waits until 2026, the exclusion amount is scheduled to be about $7 million after the TCJA sunset, meaning $3 million of the $10 million gift would be taxable. A relatively small difference in timing can result in a huge tax bill.

Before making any moves or decisions about your gifting strategy, please consult with us. It is critical to understand potential tax implications and ensure everyone involved in your estate plan, including your heirs, optimize and take advantage of the best strategies for your situation.

Wealth Transfer & a Bypass (Family) Trust

Another popular method of optimizing tax exemptions for married couples is a Bypass Trust. When one spouse passes, a portion of their assets can be placed into a trust which passes to their beneficiaries on the death of the surviving spouse. The assets placed into this trust, and any appreciation of those assets, are protected from estate taxes when the surviving spouse passes away.

This strategy, like many others in estate planning, can be complicated and the tax ramifications and appropriateness should always be discussed with a qualified estate planning attorney and financial professional prior to making any decisions.

Portability for Estate & Gift Tax

In very simple terms, portability is a way for spouses to combine their exemption from estate and gift tax. In most circumstances, it’s a process where a surviving spouse can realize and use the unused estate tax exemption of a deceased spouse, so then, the surviving spouse has both their own exemption from estate and gift tax and, the unused exemption of the deceased spouse. This can be a highly complicated process that requires filings and needs to be discussed with your financial professional and estate planning attorney.

Keeping Your Estate Plan Current – Don’t Forget the Basics!

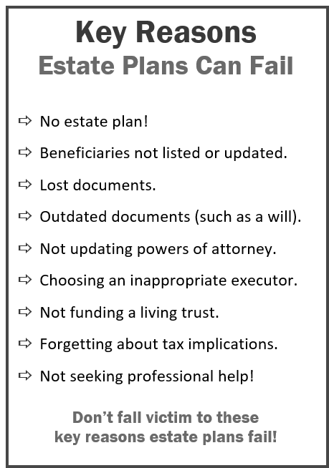

Even if your estate plan is not affected by the sunsetting TCJA provisions, it is still wise to have an updated estate plan. Life happens and not having proper documents can cause undue stress and work for your loved ones. It’s important to keep your estate plan updated. Divorces, marriages, children coming of age, new children, or grandchildren – are among the major, but easily overlooked occurrences that can directly affect your estate plan.

Revisiting your beneficiaries is important as well. Many people grow fond of new charities, individuals may no longer be appropriate candidates, or percentages may change. Confirming who you have chosen as primary and contingent beneficiaries is very important.

You’ve spent a lifetime acquiring your estate, it is important to preserve your legacy in the manner in which you desire. If you would like to review your estate plan with us, please contact our office and we would be happy to review it with you.

Use It or Lose It!

At present, the potential for you to lose your opportunity to leverage the higher exemption levels is a possible scenario. Don’t postpone your opportunity to explore the options currently available to you!

We Are Here to Help

We value our clients and are honored to be a part of their journey. We strive to understand the objectives of each individual so we can create an optimal plan.

As a reminder, please keep us aware of any changes (such as health issues, changes in your retirement goals, or the sale of a home). The more knowledge we have about your unique situation the better equipped we will be to best advise you. If you’d like to have an assessment of your investment portfolio and overall financial picture, we can discuss this at your next review meeting, or you can call us to set up an appointment.

As always, we appreciate the opportunity to assist you with all your financial needs.

We want to offer our services to other clients just like you!

Do you know someone who may benefit from this information? Please share this article with others!

Upcoming Events

- Retirement Classes | Apr-May

- Investments Webinar | Wed, Apr 24 at 6pm

- Property Inheritance Webinar | Wed, May 1 at 6pm

- Social Security & Medicare Webinar | Wed, May 8 at 6pm

- FAN Corporate Trustee Services Webinar | Wed, May 22 at 6pm