Ideas to Help Prepare for a Recession

- 30

- May

For the last several months, talk of a recession has been making news headlines. Analysts and investors have been speculating if, when, and how bad of a recession the U.S. could experience. News sources have resembled Paul Revere proclaiming, “a recession is coming!”

In their recent meetings, the Federal Open Market Committee (FOMC) reported that they expect the U.S. to experience a recession in the coming months of 2023. How long and how severe is unknown. Investor fears are becoming higher due to recent interest rate increases, inflation, and the failure of some community banks.

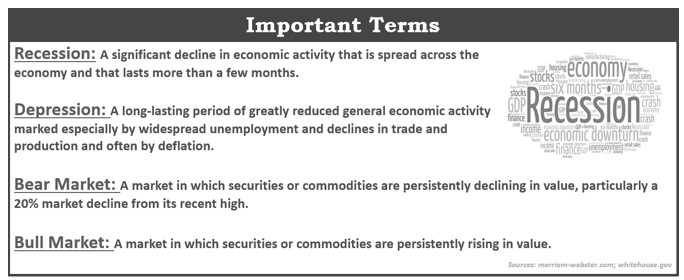

We believe an educated client is the best client, so let’s define a recession, as it could mean many different things to people. The conventional definition is that two consecutive quarters of falling real Gross Domestic Products (GDP) constitute a recession. GDP is the broadest measure of the activity and health of the economy.

According to a White House release, this is not the official definition nor the way that their economists evaluate a business cycle. “Both official determinations of recessions and economists’ assessment of economic activity are based on a holistic look at the data—including the labor market, consumer and business spending, industrial production, and incomes.

Based on these data, it is unlikely that the decline in GDP in the first quarter of this year—even if followed by another GDP decline in the second quarter—indicates a recession” (whitehouse.gov, 7/21/22). The Bureau of Economic Research’s (NBER) Business Cycling Dating Committee is the official organization that determines whether the data compiled shows the U.S. is in a recession. They define it as, “a significant decline in economic activity that is spread across the economy and that lasts more than a few months.”

Rather than argue over the definition of the term recession, let’s review some helpful information for investors. To put recessions into perspective, since 1854, there have been 33 recessions, with five of them experienced since 1980. For many of us, recency bias plays a role in our thoughts because from December 2007 to June 2009, we experienced what was called, “The Great Recession.” This recession was primarily caused by the collapse of subprime mortgages and the credit crunch in the global banking system and lending, which ensued.

As findings of that recession share, an estimated 6 million American households defaulted on high-risk housing loans. As a result of that recession, the stock market reacted dramatically. Also, during that time, the GDP fell 4.3%, which was the largest decline in 60 years, and the unemployment rate peaked at 10% in October 2009 (businessinsider; 8/8/22).

As we currently stand, we are not experiencing anything like the Great Recession. The economy is slowing down, but still growing and the GDP is still increasing (with an inflation-adjusted rate of 2.6% in the first quarter of this year). The unemployment rate is hovering around 3.4%.

Regardless of how you define a recession, investors are likely to feel the pinch of an economic downturn before the year ends.

As an investor, what should you consider for your “nest egg?” Well, the bad news is that nothing is “recession-proof.” However, there are still some things you can consider in preparing for tougher times.

Two major demographics that are impacted by a recession are investors and retirees/pre-retirees. Let’s take a brief look at some strategies each one could use to become more recession resistant.

Strategies for Investors

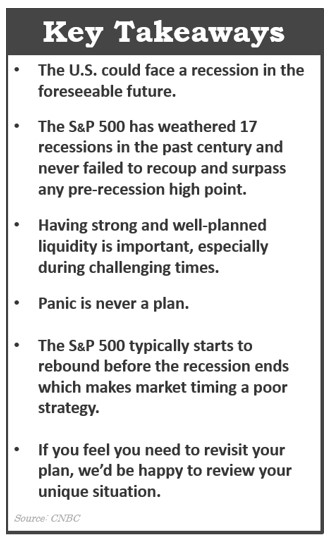

First and foremost, it is important to remember that equity markets usually start to rebound before the end of a recession. Therefore, trying to time the market can prove to be a poor investment strategy. Some things you can do include:

- Confirming your plan is still congruent with your goals. Adjusting your portfolio can have a major short- and long-term impact. You’ll need to take into consideration any changes to your time horizon, risk tolerance, and investing behavior, particularly during volatile times. If you feel you want to consider making changes to your holdings, please call us before making any adjustments.

- Review your liquidity. Tough times or downturns require an investor to be patient. In preparation for challenging times, it’s always healthy to review and set aside funds for any larger expenditures that you may have planned. Recessions are a great time to even revisit increasing if needed, your pool of liquid funds for planned activities and emergencies. Your ability to ride out a downturn can easily affect your longer-term returns.

- Look for potential entry points. Knowing things could get challenging, if you are able to do so, look during any sharp downturn for potential strategic entry points or additions into equities. Many times, downturns provide investors with great opportunities. We can help your strategy by reviewing your personal situation.

- Continue with your retirement and other regular contributions. Many investors turn to putting a hold on contributing to their retirement or savings to have more liquidity in their budget. Without the compounding of returns, this technique can put a significant roadblock to your long-term goals. First, look into discretionary expenses that you could reduce or eliminate, such as canceling subscriptions, taking fewer coffee run trips, or modifying travel plans. Try to place necessities first and then the extras!

- Don’t panic. Panic is not a plan. Unless you are “trading,” which is an intensive, higher-risk activity, don’t forget that investing is a long-term activity.

Having a long-term mindset helps investors stay more resistant to a recession. Remember why you chose the investments for your portfolio in the first place. Hopefully, you saw them as long-term holdings. As Warren Buffet said, “Nobody buys a farm based on whether they think it is going to rain the next year. They buy it because they think it is a good investment over 10 or 20 years.”

Investing for the long term means understanding that market turbulence is normal and that both downturns and recessions are a part of the long-term investment experience.

Strategies for Retirees or Pre-retirees

Many retirees have a set monthly income from pensions, social security, and retirement funds. Pre-retirees are building these sources of income so they can create a reasonable retirement lifestyle. The main objective in a recession is to maintain or continue building these funds and to try to live within the means those funds can afford.

In addition, here are some key strategies that could help retirees or those who are about to retire during challenging times.

- Understand how to live comfortably within your means. In today’s tech world, we are barraged by ads to buy things we don’t need, Amazon Prime can make it very convenient to spend money, and it can be hard to not be tempted to breach our budgets. However, it’s important to set a realistic budget and stick to it. Overspending can be a slippery slope and not one that many can afford, especially on a fixed income.

- Living mortgage and debt free. For those who can, living mortgage and debt free is an incredible opportunity to have. It reduces emotional stress and financial vulnerability during volatile times.

- Think Long Term. Most people invest in equity markets to build wealth for their retirement or personal portfolios. Regardless of your goal, investing should always be considered a long-term commitment. Did you choose investments for the long haul? Investing is a long-term activity and typically gives you a better chance at minimizing any anxieties that could be caused by short-term market noise or volatility. No matter what your time horizon is, we suggest focusing on your personal timeline instead of trying to time the market.

- Stay Healthy Mentally and Physically – Two of the biggest expenses in retirement are a mortgage and health expenses. Health expenses include not just insurance, but potential retirement and assisted living costs. Staying healthy both mentally and physically is always a goal for all of us, especially as we age.

- Understand Your Social Security Claiming Strategies. You can start receiving Social Security benefits at the age of 62, but holding off on receiving Social Security benefits beyond that age can prove to be more prosperous. For example, if you turned 62 this year, your benefits would be about 30% less than it would be should you have waited until the full retirement age of 67. You can calculate your social security benefits at the Social Security Administration’s website by going to https://www.ssa.gov/OACT/quickcalc/. For help with this, call our office and schedule a time with us.

- Don’t Panic. Again, panicking is not a wise option. We are here to help guide you through any challenges you encounter and the numerous items that need to be considered. Be careful about making changes for the sake of feeling productive or out of fear. Oftentimes, your portfolio was already well planned, and no changes are needed.

Preparation is Crucial

No matter what stage of your investing journey, one of our primary goals is to help with the preparation that is crucial to giving our clients the best opportunity for success. This is not a journey you need to go alone. Seeking out the help of a qualified financial professional who understands all the key elements necessary for a solid financial plan, including your unique financial goals, time horizon, risk tolerance, investing habits, and tax implications, is where we can add value to your journey.

If you’d like to have an assessment of your investment portfolio and overall financial picture, we can discuss this at your next review meeting, or you can call us to set up an appointment.

As always, we appreciate the opportunity to assist you with all your financial needs.

Has your financial professional discussed how a recession could affect your investments?

If you would like us to look at your personal situation and how the current market environment may affect it, please call us at (714) 597-6510 and we would be happy to schedule a complimentary discovery consultation.

Upcoming Events

Interested in attending our educational events? We have the following classes and webinars coming up in the next few months. Check out our website for more information and to register.

- Retirement Classes | Sat, Aug 19 & 26 from 8:30am to 1pm

- ID Theft Prevention Webinar | Wed, Aug 23 at 6pm

- Understanding Dementia & Alzheimer’s Disease Webinar | Wed, Sep 6 at 6pm

- Investments Webinar | Wed, Oct 4 at 6pm

- Property Inheritance Webinar | Wed, Oct 11 at 6pm

- Social Security & Medicare Webinar | Wed, Oct 18 at 6pm