.jpg)

3rd Quarter 2025 Newsletter

Resilience illustrates the ability to withstand challenges or recover quickly from difficult conditions. Resilience can also be used to describe U.S. equity performance over the past year—including the third quarter, as markets surged past record highs despite numerous potential sources of volatility.

Largely fueled by optimistic investor sentiment around the AI boom, robust corporate earnings, and expectations of further interest rate cuts, the U.S. stock market continued its bull run that began in early2023. The artificial intelligence (AI) boom is continuing to drive growth in the technology sector, dominated by the “Magnificent 7” (Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla). In addition to the AI boom, strong corporate earnings and the Fed lowering interest rates for the first time this year also helped the market rally this quarter.

The S&P 500 gained 7.79% in the third quarter, closing at 6,688.Year-to-date, as of September 30, the S&P 500 is up almost 14%. The Dow Jones Industrial Average (DJIA) closed at a record high, gained 5.22% and ended the quarter at 46,397. Year-to-date, as of September 30, the DJIA is up over 9%.

Since the recovery from the quick correction we saw in April, the market has rallied.

While the market continues to rise and investors have a bullish outlook, there is still a backdrop of caution and uncertainty. The impact of a slowing labor market, the consequences of elevated stock valuations, a possible market bubble in AI and tech stocks, and potential economic instability, can potentially dampen investor enthusiasm.

During the third quarter, the U.S. job market showed signs of cooling but remained strong. As of August, the unemployment rate was slightly elevated to 4.3%, the highest in nearly four years and a prolonged government shutdown could increase this rate in the near future (Bureau of Labor Statistics; 9/5/25).

Overall, the data continues to support a positive long-term view for equities, however there is still an under current of caution. As always, our role as financial professionals is to actively monitor developments and confirm that your portfolio remains aligned with your time horizon, risk tolerance, and financial goals. Our commitment is to keep you informed, proactive, and resilient—just like the markets themselves.

Inflation & Interest Rates

Key Points

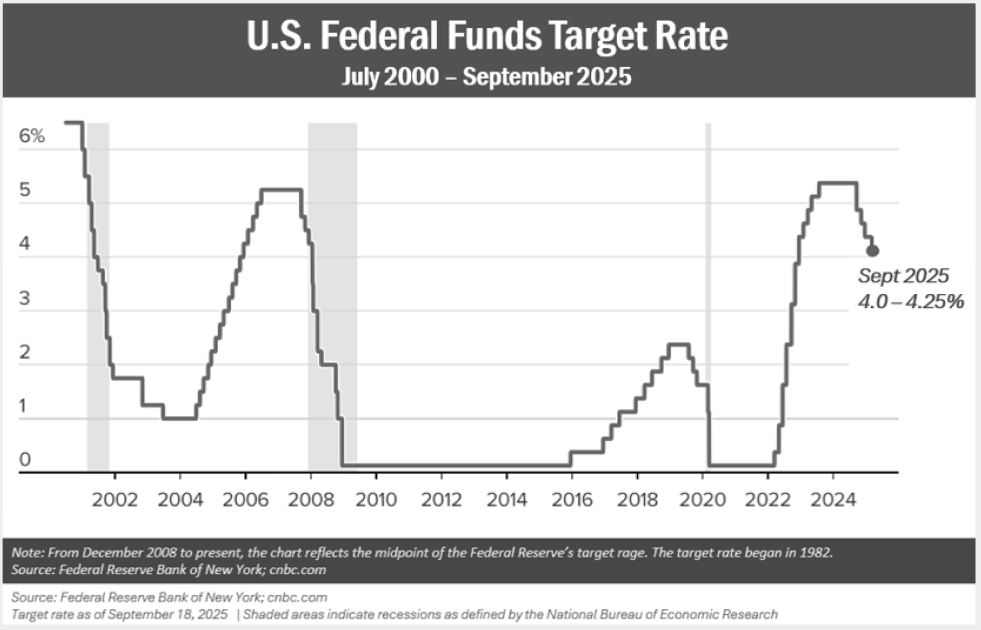

- Interest rates were lowered by 25 basis points down to 4.0 - 4.25% in September, the first rate cut for the year.

- The Fed is currently forecasting more rate cuts for 2025.

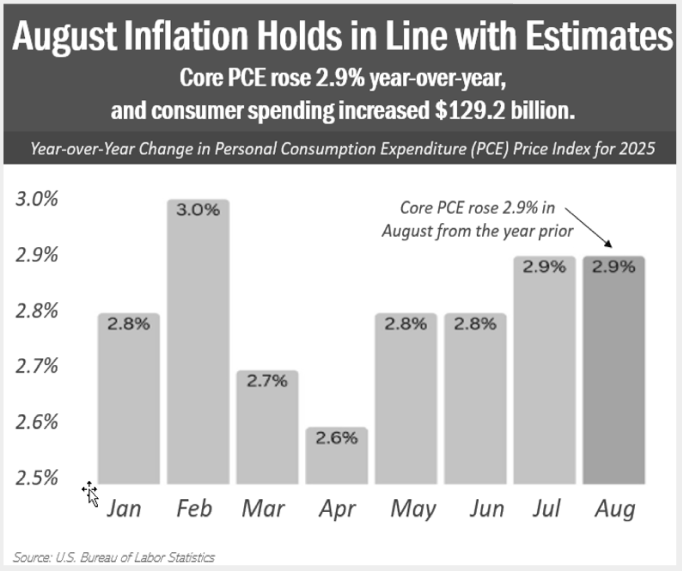

- The core Personal Consumption Expenditure (PCE) remained steady at 2.9% in August.

In its September 17, 2025, press release, the Federal Reserve noted: “Recent indicators suggest that growth of economic activity moderated in the first half of the year. Job gains have slowed, and the unemployment rate has edged up but remains low. Inflation has moved up and remains somewhat elevated” (Federal Reserve Press Release, 9/17/25).

In response to this economic landscape, the Federal Open Market Committee (FOMC) voted in September to lower interest rates for the first time in 2025, establishing a new target range of 4.0% to 4.25%. Equity markets reacted positively to this news, with major indexes reaching record highs (finance.yahoo.com,9/18/25).

Looking ahead, there are two more FOMC meetings scheduled for the remainder of 2025. While uncertainty surrounding the economic outlook persists, the Fed has indicated that additional rate cuts are possible this year, though not guaranteed. The Committee reaffirmed its long-term objectives of achieving maximum employment and 2% inflation—goals that have become challenging amidst persistent inflationary pressures and a resilient labor market. As Fed Chair Jerome Powell stated, “There is no risk-free path,” implying that aggressive cuts could fuel inflation, while maintaining high rates for too long could negatively impact unemployment (Associated Press; 9/24/2025).

In August, the core Personal Consumption Expenditure (PCE) remained steady at 2.9%. The annual Consumer Price Index (CPI) which excludes food and energy was 3.1%, according to the Bureau of Labor Statistics. Goods prices increased 0.1% while services rose 0.3%. Food showed a gain of 0.5% while energy goods and services jumped 0.8%. Housing costs posted a 0.4% rise. Consumers remain resilient despite some rising prices due to tariffs. While tariffs have created less of a threat than previously thought, their lingering effects are still a concern (cnbc.com;9/29/25).

Movements in interest and inflation rates are critical for investors' financial planning, and we will continue to closely monitor these key economic indicators.

The Bond Market & Treasury Yields

Key Points

- Bonds, which can be viewed as a safer haven for volatility, were not exempt from volatiltiiy in the third quarter.

- Like many things, the direction of bond yields remains unclear. However, with the Fed anticipating lowering interest rates this year, we could see exisiting bonds rising in value..

Bonds are typically a more stable option for investors during times of uncertainty. Lately, however, bonds have been reactive. U.S. Treasury markets responded more cautiously than equities to the Federal Reserve’s rate cut. The yield on the benchmark 10-year Treasury note briefly fell below 4% before rebounding. Bond yields ultimately moved higher, reflecting investor concerns that inflation could accelerate. Rising inflation rates the real value of future interest payments and diminishes the purchasing power of invested principal (Barron’s, 9/19/25).

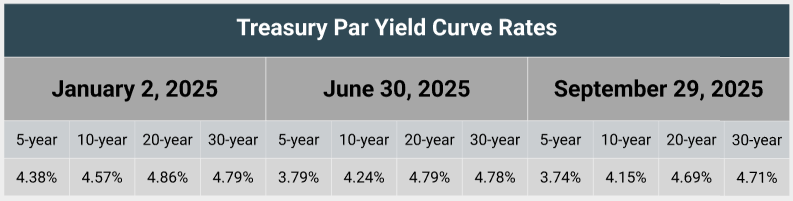

As the quarter ended, Treasury yields responded favorably to the solid data of the U.S. economy. On August 25, the 10-year Treasury yielded 4.172%, up by 2 basis points. The short-term 2-year Treasury rose to3.661% and the 30-year treasury yielded less than a basis point lower at4.749%.

The benchmark 10-year treasury yield settled at 4.12% to end the quarter, while the 20- and 30-year ended at 4.58% and 4.73% respectively (treasury.govresource center).

When bond prices rise (demand for bonds goes up), yields fall; when prices fall, yields rise. Currently, like many things, the direction of bond yields remains unclear.

We consider using bonds when they are appropriate for portfolios, and when we do, there are several things we take into consideration, including a client’s risk tolerance, time horizon, and overall investment goals. Bonds can be an integral part of a well-diversified portfolio and offer stability during times of market decline. However, please remember, while diversification in your portfolio can help you pursue your goals, it does not ensure a profit or guarantee against loss.

Investor's Outlook

Key Points

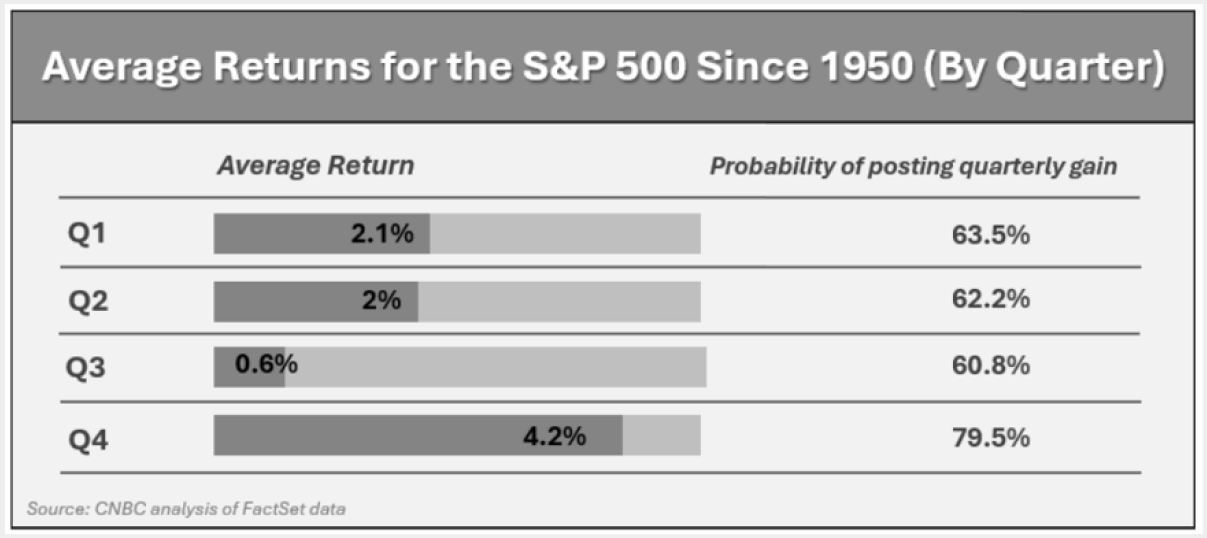

- Historically, the fourth quarter has been the strongest performing quarter for the S&P 500 since 1950.

- Vigilance is critical for the savvy investor, as volatility remains. Proceeding with caution and having a proactive planning approach that includes an emergency fund and a well-diversified portfolio that takes into consideration your risk tolerance and time horizon is still advised. A long-term approach to your financial goals and avoiding diversions is typically the best path.

While no one has a crystal ball, and past results do not reflect future ones, it’s interesting to note that based on historical data for the S&P 500 index, the fourth quarter has been the strongest-performing quarter for equities. Since 1950, it has delivered the highest average return and the highest probability of posting a gain. Seasonal factors like holiday spending, corporate earnings releases, year-end capital inflows, and portfolio rebalancing contribute to this strength (finance.yahoo.com; 9/25/25).

The chart in this report reflects returns since 1950, which includes several very difficult fourth quarters, including October of 1987 when the market collapsed and had its worst single day in history. When studying the returns, 80% of the time, the fourth quarter ended the respective year on a high note.

Many continuing uncertainties surround the economic environment, and our goal is to continue to focus on key factors that could affect your personal situation. While investor sentiment is optimistic, there are some notable risks, including overvaluation, stubborn inflation, and geopolitical tensions. Key items to continue watching as we finish the year are:

- An economic slowdown. The U.S. economy, while currently robust, is predicted to slow down. Key indicators such as labor statistics, consumer spending, and corporate earnings will help determine our economic trajectory. Although the likelihood of a deep recession is low, if growth slows more than anticipated, the risk of a recession could increase.

- The direction of inflation and interest rates. Tariffs have not significantly affected inflation as initially thought; however, inflation remains high. The Federal Reserve's goal of a 2% inflation rate continues to be elusive, and they are projecting potential interest rate cuts this year. If inflation does not moderate, the Fed may face challenges in continuing these cuts, with labor data being a critical indicator to watch.

- Overvalued Stocks. Concerns are growing that we could possibly see a modern-day version of the dot-com bubble burst from 2000. The so-called "Magnificent 7" stocks make up more than one-third of the total market capitalization of the S&P 500 and may be vulnerable to a potential bubble in AI-related stocks.

- The new tax law. The "One Big Beautiful Bill Act" was signed into law on July 4, 2025, aiming to revitalize the economy, provide tax savings for Americans, create jobs, boost domestic investment, and enhance long-term economic growth. Many taxpayers have questions about how these new tax laws may impact them. If you'd like to discuss this further, please reach out to us.

- Geopolitical conflict. The global economy remains in a delicate position, with ongoing tensions in the Middle East and the unresolved Russia-Ukraine conflict adding to the uncertainty.

As the saying goes, “Everything is fine until it’s not.” Volatility is still prevalent and may continue for some time. As we look to the future, being vigilant is crucial for savvy investors. Remember, while volatility can have negative implications, it can also present opportunities. As the investing legend Warren Buffet once said, “Be fearful when others are greedy, and greedy when others are fearful.” Therefore, we would like to remind you once again that equities are long-term investments.

2025 continues to be a year of change for the U.S. As your financial stewards, we closely monitor areas that we believe are important to your financial well-being. We understand that these changes can bring uncertainty, and we believe an informed client is the best kind. We will keep you updated on developments that could impact your personal situation.

As always, please inform us of any changes to your circumstances, including health issues, the sale of property, or adjustments to your risk tolerance or time horizon. We encourage you to share any concerns, ideas, or potential decisions with us before taking action. Financial choices often have tax implications and other considerations, therefore, the more we understand your unique situation, the better positioned we are to offer tailored guidance.

Our commitment is to exceed your expectations by delivering exceptional service and maintaining consistent, meaningful communication throughout the year. Our team is here to help you with every step of your journey toward your financial goals. Please feel free to reach out to us with any questions or concerns you may have. We greatly value the trust and confidence you place in our firm and look forward to continuing to serve you.

We are accepting new clients

- Do you feel your advisor is fully aware of your financial situation?

- Are you satisfed with how your advisor is keeping you updated?

- Has your advisor reviewed your tax forms to understand how to coordinate your investments with your taxes?

- Has your advisor discussed tax planning strategies that could help you keep more of what you make>

- Is your advisor updated and current on tax planning strategies?

- Would you like a complimentary review of your financial situation?

If you answered No or Not Sure to any of these questions, we would like to offer you a complimentary private consultation with one of our professionals at no cost or obligation to you. To schedule your financial consultation, please call us at (714) 597-6510 or info@fanwmg.com.

Upcoming Events

- Understanding Dementia & Alzheimer's Disease Webinar | Wed, Oct 22 at 6:00pm

- Tax Update Webinar | Wed, Oct 29 at 6:00pm

- FAN Food Drive | November

- FAN Plan Basic Training Webinar | Wed, Dec 3 at 6:00pm

- Retirement Classes | Jan- Feb

Click HERE to learn more about our upcoming events.

Note: The views stated in this letter are not necessarily the opinion of Financial Advisors Network, Inc. and should not be construed, directly or indirectly, as an offer to buy or sell any securities mentioned herein. Investors should be aware that there are risks inherent in all investments, such as fluctuations in investment principal. With any investment vehicle, past performance is not a guarantee of future results. Material discussed herewith is meant for general illustration and/or informational purposes only, please note that individual situations can vary. Therefore, the information should be relied upon when coordinated with individual professional advice. This material contains forward-looking statements and projections. There are no guarantees that these results will be achieved. All indices referenced are unmanaged and cannot be invested into directly. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment. There is an inverse relationship between interest rate movements and bond prices. Generally, when interest rates rise, bond prices fall and when interest rates fall, bond prices generally rise. There is no guarantee that a diversified portfolio will enhance overall returns outperform a non-diversified portfolio. Diversification does not protect against market risk.

The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. Stock market. The modern design of the S&P 500 stock index was first launched in 1957. Performance prior to 1957 incorporates the performance of the predecessor index, the S&P 90. Dow Jones Industrial Average (DJIA), commonly known as “The Dow” is an index representing 30 stocks of companies maintained and reviewed by the editors of the Wall Street Journal. Past performance is no guarantee of future results. CDs are FDIC Insured and offer a fixed rate of return if held to maturity. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed.

Sources: cnbc.com; barrons.com; marketwatch.com; treasury.gov; Bureau of Labor Statistics; Federal Reserve; The Associated Press; U.S. Department of Treasury. Contents provided by the Academy of Preferred Financial Advisors,2025.

Turn Bulletins into Action

Stay informed—then come in for a free consultation and see how the updates apply to your financial life.