.png)

2nd Quarter 2026 Newsletter

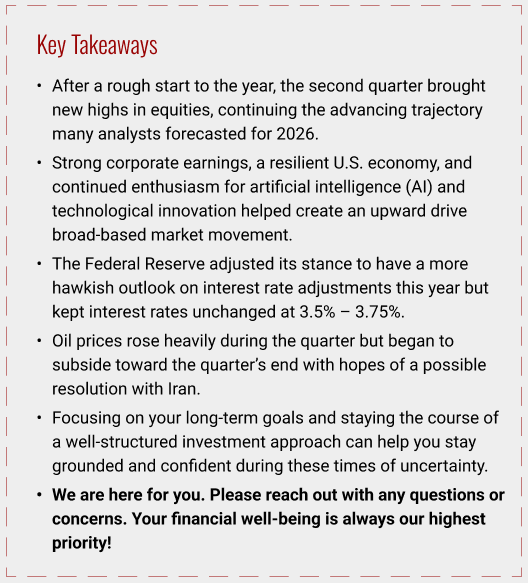

The second quarter of 2026 demonstrated an important lesson for investors: markets can continue to advance even when uncertainty dominates the headlines. Persistent inflation concerns, heightened geopolitical tensions, high energy prices, and evolving expectations for Federal Reserve policy all contributed to periods of market volatility. Despite these headwinds, U.S. equities recovered from a difficult first quarter and continued their longer-term upward trend, leaving the major market indices higher after the first half of the year. Once again, equity markets recorded new highs during the quarter.

Following a volatile first quarter, investor confidence strengthened during the second quarter. Strong corporate earnings, a resilient U.S. economy, and continued enthusiasm for artificial intelligence (AI) and technological innovation helped drive a broad-based equity market recovery.

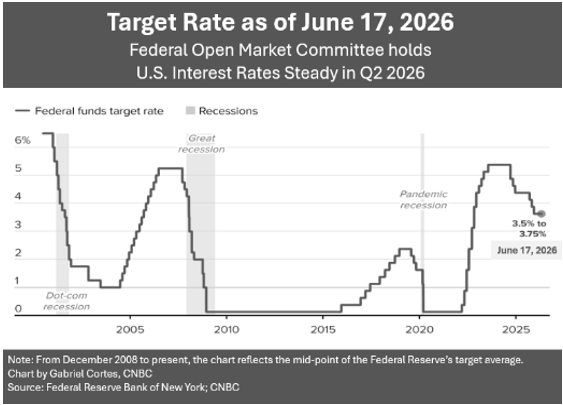

Equity markets also navigated an important leadership transition at the Federal Reserve. Following the departure of Chair Jerome Powell, Kevin Warsh presided over his first Federal Open Market Committee (FOMC) meeting. As widely expected, policymakers left the federal funds target range unchanged at 3.50% to 3.75%. While interest rates remained steady, the Committee adopted a more hawkish tone, signaling that inflation still remains a primary concern and they reduced expectations for possible interest rate cuts later this year.

After a down first quarter, both the S&P 500 and DJIA indexes made impressive rebounds. The S&P 500 closed the quarter at 7,499.36 up 14.4%. The Dow Jones Industrial Average closed the quarter at 52,319.20, gaining approximately 12.8% for the quarter (statmuse.com).

Through the first six months of 2026, the S&P 500 has gained 9.6%, and the Dow has advanced 8.9% (apnews.com; 6/30/26).

One of the most important drivers of equity markets is the direction of corporate America – and it continued to deliver solid results. According to FactSet, on June 26, the estimated year-over-year growth for S&P 500 companies is 23.1%, which would mark the seventh consecutive quarter of double-digit earnings increases and the second-straight quarter of earnings growth over 20%. Technology companies remained market leaders, driven by continued demand for artificial intelligence and digital infrastructure, while the energy sector benefited from sharply higher oil prices during much of the quarter.

The energy sector was among the largest contributors to market volatility. West Texas Intermediate (WTI) crude oil surged to over $110 per barrel amid escalating geopolitical tensions and concerns over potential supply disruptions. As tensions eased later in the quarter, crude oil prices retreated to approximately $70 per barrel, helping relieve some inflationary pressure and improving investor sentiment. (Source: ycharts.com)

The U.S. labor market continued to demonstrate resilience. According to the U.S. Bureau of Labor Statistics, the unemployment rate remained steady at 4.3% in May, reflecting continued labor market stability despite signs of moderating economic growth.

Overall, the second quarter reinforced an important investment principle: while headlines often create short-term market volatility, long-term market performance is ultimately driven by healthy, long-term focused fundamentals. During the quarter, potential catalysts for market downturns were balanced by factors that continued to support economic growth and a healthy investment environment. These competing forces underscored that volatility remains a normal part of investing, while reinforcing the importance of focusing on long-term fundamentals rather than reacting to short-term market noise.

As market conditions continue to evolve, maintaining a disciplined, well-structured investment approach remains essential. As financial professionals, our role is to closely monitor market developments and help ensure your portfolio remains aligned with your broader financial goals. We remain committed to keeping you informed, prepared, and well-positioned to navigate changing market conditions with confidence.

Inflation & Interest Rates

Key Points:

- The Federal Reserve left the federal funds rate unchanged during the second quarter of 2026, maintaining the target range at 3.50%–3.75%.

- Inflation remains above the Fed's long-term target and continues to be a primary concern.

- The Federal Open Market Committee (FOMC) has adopted a more hawkish stance, reducing expectations for rate cuts and signaling the possibility of future rate increases.

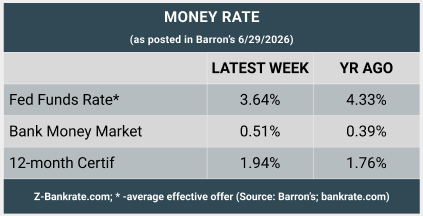

During the first half of 2026, the Federal Open Market Committee (FOMC) kept its benchmark federal funds rate unchanged, maintaining the target range at 3.50%–3.75%, leaving borrowing costs the same for five consecutive meetings.

At the April FOMC meeting, the final meeting chaired by Jerome Powell, the Federal Reserve held interest rates steady. This decision was widely anticipated amid persistent inflationary pressures fueled in part by elevated global energy prices.

The June meeting marked the first FOMC gathering under newly appointed Federal Reserve Chair Kevin Warsh. Policymakers again voted to maintain the target rate range of 3.50%–3.75%, while signaling a more hawkish outlook for the remainder of the year. According to updated projections, nine of the eighteen committee members now expect at least one rate increase before year-end, and previous indications of potential rate cuts have largely been removed. (Source: CNBC, June 17, 2026)

In its June policy statement, the FOMC noted: "Economic activity is expanding at a solid pace despite elevated uncertainty that owes, in part, to the conflict in the Middle East. Productivity growth and capital investment are strong. Job gains have kept pace with the workforce, and the unemployment rate has changed little."

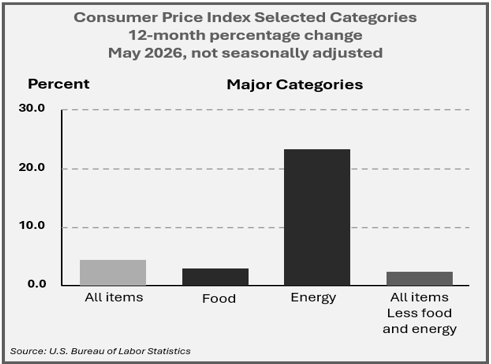

Consumer spending also remains healthy. According to May data from the Bureau of Labor Statistics, the core Consumer Price Index (CPI), which excludes food and energy, increased 2.9% year-over-year. Food prices rose 3.1%, while shelter costs, the largest component of the CPI, increased 3.4% from a year earlier. (Source: Bureau of Labor Statistics)

The June meeting also brought updated inflation forecasts. In March, FOMC members projected that the Personal Consumption Expenditures (PCE) Price Index would end 2026 at an annual rate of 2.7%. By June, that estimate had been revised upward to 3.6%, while core PCE, which excludes food and energy prices, was projected to finish the year at 3.3%. (Source: CNBC, June 17, 2026)

Looking ahead, currently the prospect of a rate cut in 2026 appears increasingly unlikely. In fact, the possibility of a rate increase later this year has gained momentum. The path forward will largely depend on the trajectory of inflation, labor market conditions, and overall economic growth.

Geopolitical developments may also influence inflation trends. As of late June, negotiations toward a potential framework for peace between Iran and the Trump administration were reportedly underway. Should an agreement be reached, lower crude oil prices could help ease energy-related inflationary pressures.

Interest rates and inflation remain critical factors in financial planning and investment decision-making. We will continue to monitor these economicindicators closely and provide updates as conditions evolve.

The Bond Market & Treasury Yields

Key Points:

- Treasury yields remained elevated as investors continued to consider the prospect of higher-for-longer interest rates.

- The Treasury yield curve continued its gradual normalization following an extended period of inversion.

During the second quarter of 2026, U.S. Treasury yields remained elevated as investors assessed persistent inflation, resilient economic growth, and evolving expectations for Federal Reserve monetary policy. While Treasury yields experienced short periods of volatility, particularly in response to economic data releases and shifting interest rate expectations, the bond market remained relatively resilient as investors balanced inflation concerns against continued signs of economic strength.

Throughout the quarter, the 10-year Treasury yield generally traded in the mid-4% range, while the 2-year Treasury yield remained above 4%, reflecting expectations that short-term interest rates would stay higher for longer.

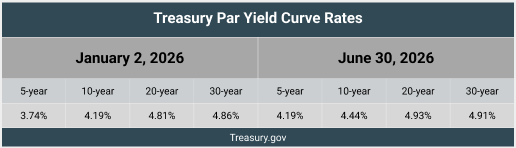

At the end of the second quarter, the 10-year Treasury yield closed at 4.44%, the 5-year Treasury yield at 4.19%, and the 30-year Treasury yield at 4.91%. (Source: U.S. Department of the Treasury Resource Center)

After remaining inverted for much of the previous two years, the Treasury yield curve continued normalizing during the quarter. The spread between shorter- and longer-term Treasury yields moved into positive territory, suggesting investors anticipate continued economic expansion alongside a more balanced long-term interest rate environment.

Although expectations for the timing and pace of future interest rate adjustments continued to shift, Treasuries and bonds remain an important component of diversified investment portfolios. They may offer a relatively more stable alternative to equities, particularly during periods of heightened market uncertainty. At the same time, the possibility of rising interest rates could create price volatility for existing bonds. Please remember that while diversification in your portfolio can help you pursue your goals, it does not ensure a profit, or guarantee against loss.

As always, bond investments should be evaluated within the context of an investor’s risk tolerance, time horizon, and overall financial objectives. Bonds remain a core component of many well-balanced portfolios, and we will continue to monitor developments, Federal Reserve policy and Treasury markets as conditions evolve.

Oil

Key Points:

- National average gasoline prices increased nearly 32% during the second quarter of 2026.

- Easing geopolitical tensions late in the quarter contributed to a decline in crude oil and gasoline prices.

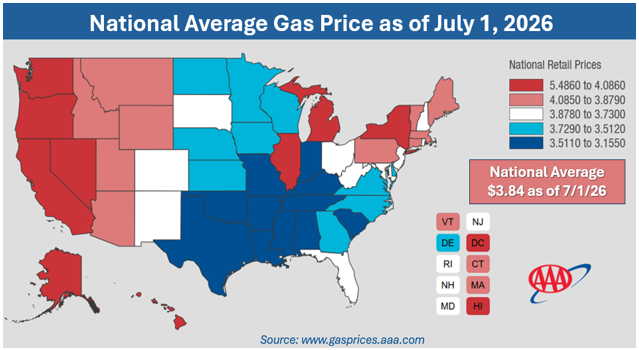

National gasoline prices increased significantly during the second quarter of 2026. After averaging approximately $2.98 per gallon at the end of February, the national average climbed to approximately $4.56 per gallon by mid-May. Higher crude oil prices, coupled with geopolitical tensions in the Middle East, contributed to the rise in fuel costs. (Source: gasprices.aaa.com)

As the quarter neared its end, oil prices started to moderate as geopolitical tensions eased at the prospect of avoiding more major disruptions to global energy supplies. Because the Middle East remains a critical source of global oil production and exports, developments in the region continue to have a meaningful influence on energy prices and investor sentiment.

While recent declines in oil prices have provided some relief, uncertainty remains. Future negotiations and geopolitical developments could either support additional price stabilization or lead to renewed volatility if supply concerns reemerge. Lower energy prices, if sustained, could help moderate inflationary pressures, improve consumers' purchasing power, and provide additional support for economic growth.

At the end of the second quarter, oil prices retreated back toward the pre-conflict levels. Global benchmark Brent crude fell below $73, a much more manageable number than the April highs of over $125 per barrel. (Sources: cnn.com; bbc.com)

We will continue to monitor developments in global energy markets and assess their potential impact on inflation, interest rates, corporate earnings, and overall market performance.

Investor's Outlook

Key Points:

- We remain cautiously optimistic. While volatility is likely to remain, continued earnings growth, a resilient economy, and the possibility of a resolution in Iran, provides an encouraging backdrop for investors as we move through the remainder of 2026.

- Maintaining a long-term focus and avoiding short-term distractions has been one of the most effective ways to pursue financial goals.

As we enter the second half of 2026, the investment landscape remains, for the most part, positive, although investors should continue to expect periods of elevated volatility. The same factors that influenced markets during the first half of the year are likely to remain the primary drivers of market performance:

- the direction of inflation,

- Federal Reserve policy,

- corporate earnings,

- geopolitical developments, particularly regarding the Strait of Hormuz,

- confidence in advancements in technology and artificial intelligence.

Looking ahead, we remain cautiously optimistic. Although volatility is expected, the combination of healthy corporate earnings and a resilient economy provides a supportive backdrop for investors as we move through the remainder of 2026.

Most analysts are suggesting higher movements in equity markets when deliberating the outlook for the remainder of 2026. Ed Yardeni, the President of market advisory firm Yardeni Research and former Chief Investment Strategist at Deutsche Bank's U.S. equities division, expects the stock market to continue its rise over the second half of this year and is forecasting a further 9% gain in the S&P 500. To the contrary, a handful of others, including Tyler Richey, an analyst at Sevens Report Research, are predicting a decline in major indexes through the end of 2026. (Source: abcnews.com; 6/30/26)

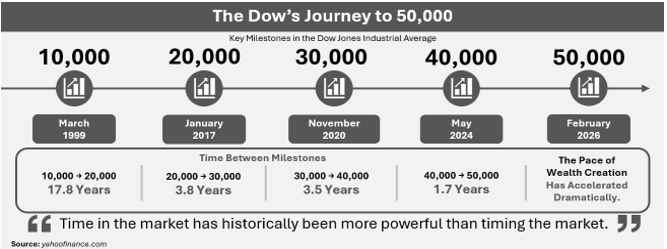

The pace of equity market growth has accelerated over the last decade, however, we are not in the business of predicting the future. Regardless of what may transpire, history has consistently demonstrated that maintaining a disciplined, diversified investment strategy remains one of the most effective ways to navigate uncertain markets. Rather than attempting to predict short-term movements, or falling prey to the day-to-day noise from the media, investors are generally better served by remaining focused on their long-term financial objectives and allowing high-quality investments time to compound. We will continue to closely monitor market developments and make thoughtful portfolio adjustments when appropriate, always with your long-term goals at the forefront of our investment decisions.

Short-term volatility is likely to remain. Please remember that volatility is a normal and expected part of the investment experience. While market fluctuations can feel uncomfortable, they are not always negative and may create opportunities for disciplined investors. Periods of market weakness can bring the ability to invest at more attractive prices, rebalance portfolios, or harvest losses to help offset capital gains. As always, portfolios should be thoughtfully selected and aligned with each investor’s unique objectives, time horizon, and risk tolerance.

We believe an informed client is the best client. Our commitment is to exceed our clients’ expectations by delivering exceptional service, maintaining consistent and meaningful communication throughout the year, and proactively planning to help clients navigate the changing economic environment. We will keep clients informed about developments that could impact their personal situation, and as always, we encourage clients to inform us of any changes to their circumstances, risk tolerance, or time horizon.

Our team is here to help clients with every step of their journey toward their financial goals. We would welcome the opportunity to help you with your financial decisions. Please feel free to reach out to us with any questions or concerns you may have.

.png)

We are accepting new clients!

- Do you feel your advisor is fully aware of your financial situation?

- Are you satisfied with how your advisor is keeping you updated?

- Has your advisor reviewed your tax forms to understand how to coordinate your investment with your taxes?

- Has your advisor discussed tax planning strategies that could help you keep more of what you make?

- Is your advisor updated and current on tax planning strategies?

- Would you like a complimentary review of your financial situation?

If you answered No or Not Sure to any of these questions, we would like to offer you a complimentary, private consultation with one of our professionals at no cost or obligation to you. To schedule your financial consultation, please call us at (714 ) 597-6510 or email info@fanwmg.com.

Upcoming Events

- Retirement Classes | Sep - Oct

- ID Theft Prevention Webinar | Wed, Sep 2 at 9pm PT

- Investments Webinar | Wed, Oct 7 at 6pm PT

- Property Inheritance Webinar | Wed, Oct 14 at 6pm PT

- Social Security & Medicare Webinar | Wed, Oct 21 at 6pm PT

- Understanding Dementia & Alzheimer's Disease Webinar | Wed, Oct 28 at 6pm PT

- Tax Planning & Update Webinar | Wed, Nov 4 at 6pm PT

Click HERE to learn more about our upcoming events.

Financial Advisors Network, Inc. is a registered investment advisory firm. Note: The views stated in this letter are not necessarily the opinion of Financial Advisors Network, Inc., and should not be construed, directly or indirectly, as an offer to buy or sell any securities mentioned herein. Investors should be aware that there are risks inherent in all investments, such as fluctuations in investment principal. With any investment vehicle, past performance is not a guarantee of future results. Material discussed herewith is meant for general illustration and/or informational purposes only, please note that individual situations can vary. Therefore, the information should be relied upon when coordinated with individual professional advice. This material contains forward-looking statements and projections. There are no guarantees that these results will be achieved. All indices referenced are unmanaged and cannot be invested into directly. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment. There is an inverse relationship between interest rate movements and bond prices. Generally, when interest rates rise, bond prices fall and when interest rates fall, bond prices generally rise. There is no guarantee that a diversified portfolio will enhance overall returns outperform a non-diversified portfolio. Diversification does not protect against market risk.

The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. stock market. The modern design of the S&P 500 stock index was first launched in 1957. Performance prior to 1957 incorporates the performance of the predecessor index, the S&P 90. Dow Jones Industrial Average (DJIA), commonly known as “The Dow” is an index representing 30 stocks of companies maintained and reviewed by the editors of the Wall Street Journal. Past performance is no guarantee of future results. CDs are FDIC Insured and offer a fixed rate of return if held to maturity. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed.

Sources: Barron’s; apnews; statmuse.com; cnbc.com; gasprices.aaa.com; nytimes.com; cnn.com; bbc.com; investing.com; factset.com; yahoofinance.com; U.S. Department of Treasury. Contents provided by the Academy of Preferred Financial Advisors, 2026

Turn Bulletins into Action

Stay informed—then come in for a free consultation and see how the updates apply to your financial life.