.jpg)

2nd Quarter 2025 Newsletter

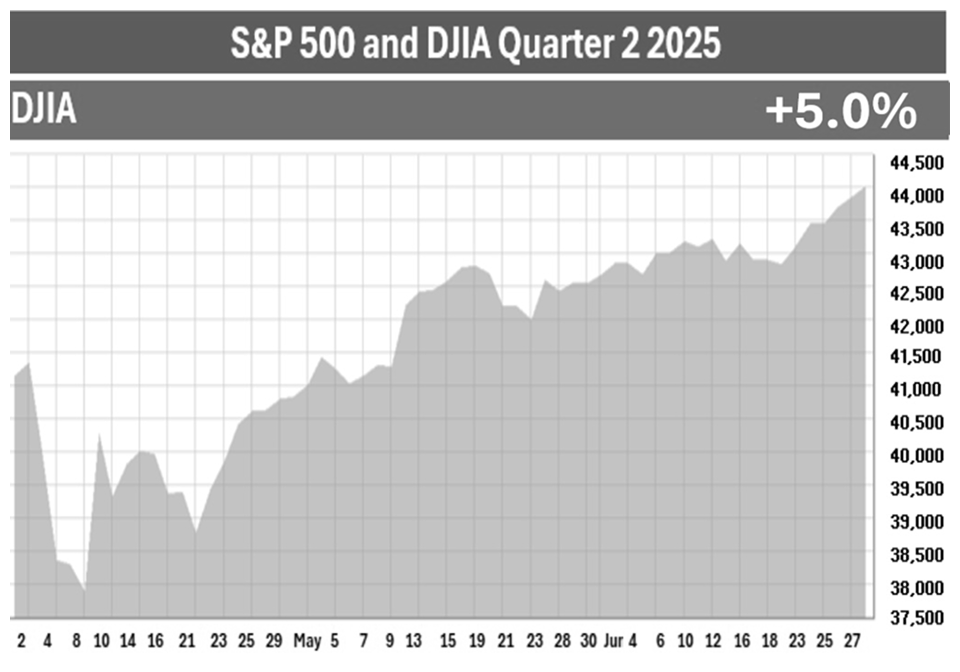

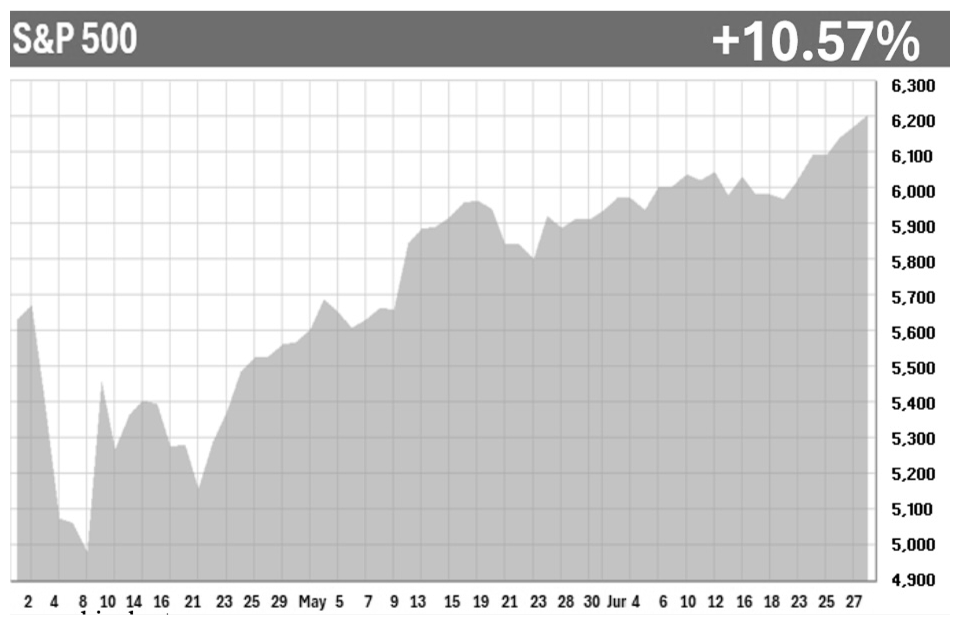

Almost every investor has heard the saying, “equities are for long-term investors.” This philosophy was reinforced in the first half of 2025, which witnessed significant and historical changes in equity movements. If you left Earth on January 1 and returned on June 30, you would see that the S&P 500 started the year on ahigh note and achieved a new high on June 30. This is great news for investors.

However, the first half of this year has also been one of the most volatile first halves ever, with the market experiencing a correction of nearly 20% before rebounding to reach a new high.

As the second quarter began, many analysts downgraded their annual forecasts, predicting potential doom and gloom for investors for the remainder of 2025. In early April, when people thought the world would collapse and the market dipped below 5,000, the outlook seemed bleak.

Since then, the market has rallied. By early May, it regained its year-to-date losses and entered positive territory for the year. After advances of approximately 5% in both May and June, the S&P 500 closed the second quarter at all-time highs, leaving investors who stayed with equities feeling joyful once again.

The new administration and President Trump came into office with full disclosure that he planned on rocking the boat. Change can lead to uncertainty during transitions and the recent dramatic ups and downs have left investors with their seats buckled and wary of any sudden moves.

Throughout the second quarter, equities remained volatile but found a bottom when investors saw hefty initial tariff plans announced back in April. As you can see from the charts on page one, the road had some bumps on the way back up from correction land and several major factors continued to put pressure on equities. These included pending tariff policies, reluctant inflation rates, potential economic slowdown, and geopolitical conflicts.

After a lot of turbulence in the equity markets, geopolitical conflicts took centerstage at the end of the quarter, leading to an attack on Iranian nuclear sites. Investors were spared as U.S. equities were unphased by the strike. To the contrary, equities rose slightly the following Monday. Some feel this was an example of how “headline events are having less and less effect on the market since tariffs went on - the so-called Liberation Day - which was the big volatile event,” according to Andrew Wells, San Jac Alpha’s Chief Investment Officer.

During late June, even tariffs took a side burner to geopolitical conflict in the news. However, the current tariff pause, as of the writing of this newsletter, is set to end in the next few weeks and talk of reciprocal tariffs is on the table for most countries. We remain committed to keeping a watchful eye on tariffs and their effects on our client’s investment portfolios and financial plans.

Despite all these challenges, equities powered through and hit all-time highs to end the quarter. The S&P 500 closed the quarter at a record high of 6,203.31,up 10.57%, and posted its best quarter since December 2023. The S&P 500 was up 24.5% since a low hit on April 8 and is up 5.5% on the year as of June 30 (cnn.com; 6/30/25).

The Dow Jones Industrial Average (DJIA) closed the quarter at 44,077.26, up 5%. For the year, the DJIA is up 3.6%.

With equities remaining strong, many analysts believe that the rally we experienced following the correction (a decline of more than10% from a recent closing high) is not merely a bear market rally, but a trend toward new highs. As noted, the S&P 500 reached a new high at the end of this quarter, as did the tech-heavy NASDAQ.

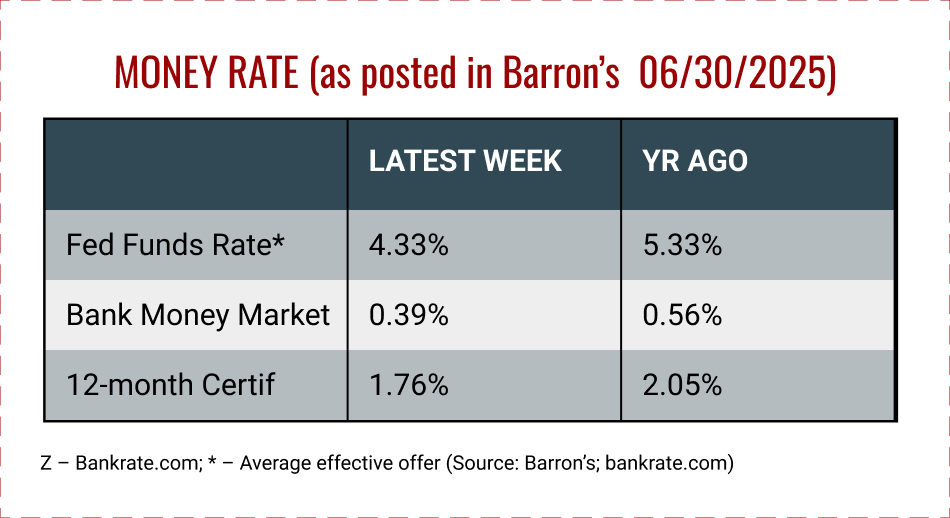

Investors still have not seen any interest rate cuts from the Fed in 2025. The Federal Open Market Committee (FOMC) decided to maintain steady interest rates during the first and second quarter of 2025. Current Federal Funds interest rates are in the range of 4.25% to 4.50%.

During the June FOMC meeting, Feds still projected two rate cuts this year. For now, Federal Reserve Chair Jerome Powell noted they are, “well positioned to wait” before making any moves on rates (cnbc.com; June 18, 2025).

In both April and May, the unemployment rate was a healthy 4.2%. Government employment continued to go down and is anticipated to remain in this direction as those employees who are currently on paid leave or receiving severance are still considered employed until the duration of the paid leave or severance ends. In June the unemployment rate came in better than expected and fell to 4.1%.

2025 continues to be a year of change. While many signs are strong, others are cautionary. As financial professionals, we are committed to keeping our clients aware of any changes that could directly affect their situation. Our goal is to consistently review our clients’ investments and confirm they align with their time horizon, risk tolerance and goals.

Key Takeaways

- After a very volatile first quarter that took equities into correction territory, equities recovered in teh second quarter and ended it at record highs.

- Trade tensions, tax law changes, and heightened geopolitical conflict are amongst the top antognists of continued uncertainty and volatility.

- The Fed held the federal funds rate range steady at 4.25 - 4.5%. The Fed is still anticipating two rate cuts this year.

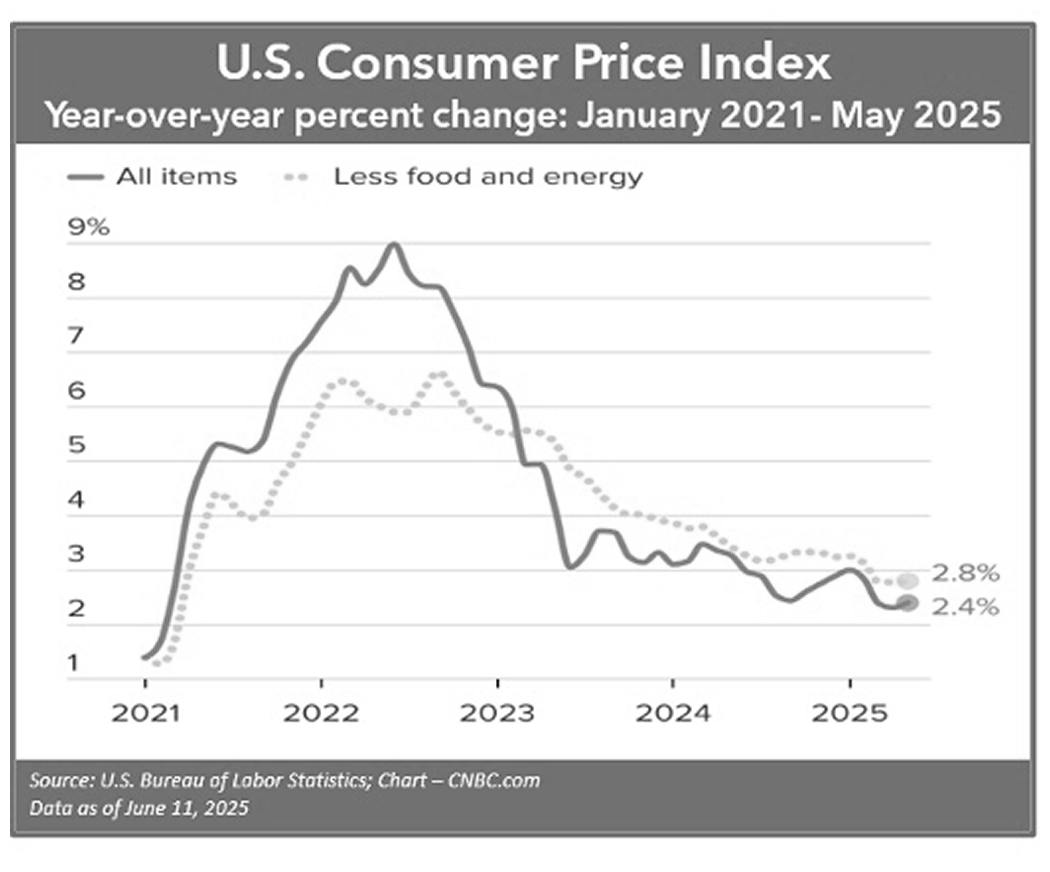

- Overall, inflation remained trending in the desired direction in the second quarter. In April and May, the core CPI held steady at 2.8%.

- While bonds present a less risky alternative to equities and an additional option for those looking to diversify their portfolio, they still experienced some volatiltiy.

- Focusing on your long-term goals and staying the course of a well-guided plan can help you stay grounded and confident during these times of uncertainty.

- We are here for you to discuss any questions or concerns you may have.

Inflation & Interest Rates

Key Points:

- Interest rates remained unchanged at 4.25 – 4.50% during the second quarter of 2025.

- The Fed is still forecasting rate cuts for 2025.

- U.S. inflation decreased in May to 2.4%, slowly inching closer toward the Fed’s 2%target.

In the Federal Reserve Press Release on June 18, 2025, the committee stated, “recent indicators suggest that economic activity has continued to expand at a solid pace. The unemployment rate remains low, and labor market conditions remain solid. Inflation remains somewhat elevated” (Federal Reserve Press Release; 6/18/25).

In light of this data, during the second quarter of 2025, the Federal Open Market Committee (FOMC) decided to maintain interest rates in the range of 4.25% to 4.50%. This news did not affect investor sentiment, and stocks remained steady following the announcement.

The FOMC is vigilant in monitoring key economic indicators, including labor market conditions and inflation pressures. There are still four more meetings scheduled for 2025, however, until the trade policy is finalized, even if the labor market remains strong, a holding pattern for interest rates could remain. The Federal Reserve indicated that rate cuts are still possible this year, but Fed Chair Powell stated, “For the time being, we are well positioned to wait to learn more about the likely course of the economy before considering any adjustments to our policies,” during his post-June meeting news conference (cnbc.com; 6/18/25).

In May, the Consumer Price Index (CPI) on a year-by-year basis was 2.4% and core inflation was 2.8%. The core CPI, which excludes food and energy prices, is often viewed by economists as a better gauge of future inflation. Many anticipate that impending tariffs could reignite inflation in the coming months. We are watching how the economy is affected by tariffs, but for now, the economy has not seen any major changes due to tariffs.

Interest and inflation rate movements are integral for investors' financial planning, and we will continue to monitor these key economic indicators closely.

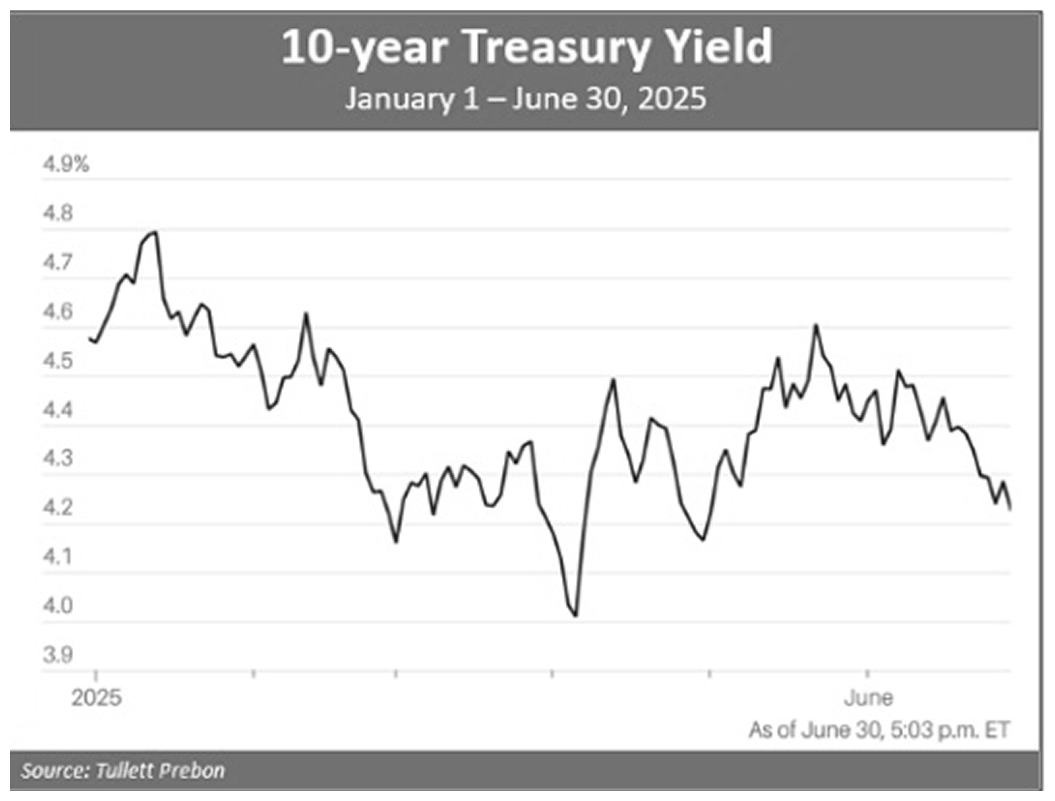

The Bond Market & Treasury Yields

Key Points:

- Bonds, while typically used as a safe haven to volatility, were not exempt from volatility in the second quarter, and they remain sensitive to continued uncertainty.

- With the Fed still anticipating lowering interest rates this year, existing bonds may rise in value.

Bonds, while typically seen as a more secure option for investors during times of uncertainty, were not exempt from volatility. Typically, bonds present a “boring ”and less risky option for investors.

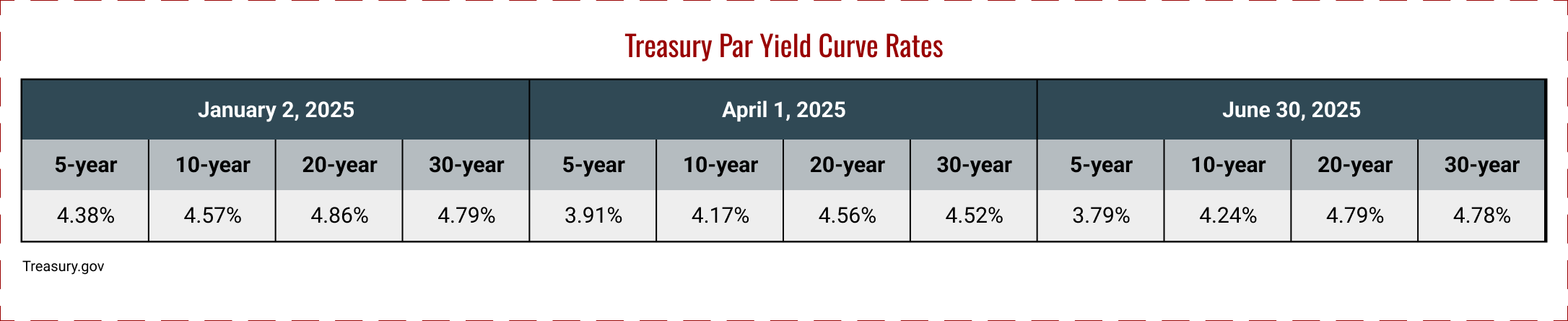

However, tariff uncertainty and a rising national debt weakened confidence in bond holders. Treasury bonds saw a decline, sending bond yields rising. Two days after “liberation day”, the 10-yearpar yield curve rate fell to 4.01% and the 20-year dropped to 4.44%. However, on May 21, the 10-year par yield curve rate was 4.58%, and the 20-year reached 5.08%.Yields then fell again as tension between the U.S. and Iran escalated. The20-year note ended the quarter at 4.79% and the 10-year note ended at 4.24%.

According to the Financial Times, investors have been dipping out of long-term U.S. bonds at the fastest rate since the COVID 19 pandemic, reflecting a backdrop of uncertainty about the future.

Like many things, the direction of bond yields remain unclear. Many factors affect them, including the movement of interest rates and inflation, geopolitical risk, and trade tensions. In particular, as it currently stands, the recently passed “One Big Beautiful Bill Act” could add over $3 trillion to the federal deficit over the next decade. The federal government issues bonds as a way to borrow money and finance the government’s operations. Hopefully, growth from tax cuts and higher tariffs could help counterbalance that debt.

We consider using bonds when they are appropriate for portfolios, and when we do, there are several things we take into consideration, including a client’s risk tolerance, time horizon, and overall investment goals. Bonds can be an integral part of a well-diversified portfolio and a good forcefield against market volatility. Bonds can offer stability and a steady interest income during times of market decline. Please remember, while diversification in your portfolio can help you pursue your goals, it does not ensure a profit or guarantee against loss.

Investor’s Outlook

Key Points:

- While they had their fair share of volatility, stocks and bonds were positive for the quarter. Looking ahead, several key factors will continue to contribute to potential uncertainty and volatility.

- Regardless of what the remainder of the year brings, proactive planning with a well-diversified portfolio that takes into consideration your risk tolerance and time horizon is still advised.

- Along-term investing strategy can help you during periods of short-term fluctuations and staying the course for your financial goals is typically the best path.

Several key factors will continue to contribute to uncertainty and volatility. Lately, a sizeable amount of the market’s gains have followed talks about the de-escalation of tariffs. Looming deadlines and lack of defined terms can keep economic uncertainty high not just for Americans, but globally. Other significant issues for equities, all of which we are monitoring, include:

- As of the quarter’s end, the economy has remained strong, but the U.S. economic growth could slow down through the rest of this year due to tariffs and government spending reductions. As of this report, the labor market was still strong.

- Inflationary pressures and results could rise during the near future due to reciprocal tariffs.

- The Fed is still projecting to lower interest rates this year.

- The “One Big Beautiful Bill Act” was signed into law on July 4, 2025. Itis hoped that this bill will help jumpstart the economy, benefit Americans by saving on taxes, be a catalyst for job creation, increase domestic investment and improve our long-term economic growth outlook.

- Global conflict remains. An escalation of the Isreal-Iran conflict could affect oil prices. In addition, the Russia-Ukraine war still continues.

As of the writing of this newsletter, tariff and trade negotiations are expected to be revisited. These negotiations will hopefully provide some definitiveness to our economic policy and the overall economic environment. Investors sentiment ended the second quarter primarily optimistic, as tariff discussions appeared to be less disruptive, including Canada rescinding its initial digital services tax that would have directly impacted Amazon, Alphabet (Google’s parent company), and Facebook.

The full impact on tariffs is yet to be seen for the American household and corporate earnings. “It takes some time for tariffs to work their way through the chain of distribution to the end consumer. A good example of that would be goods being sold at retailers today may have been imported several months ago before tariffs were imposed,” stated Fed Chair Jerome Powell. How much inflation and how expansive it is on goods is yet to be seen for U.S. consumers.

On the very first day of the third quarter, the U.S. Senate passed President Trump’s tax and spending bill and on July 3, the “One Big Beautiful Bill” Act was passed by Congress. On July4, this new act was signed into law. We will be addressing this bill and its impact in later communications.

While staying aware of economic data and news is important, please keep in mind that minimizing your exposure to inflammatory media and speculative news reports can help reduce anxiety. We believe an educated client is the best client and will keep you updated on areas that we feel could affect your personal situation.

Volatility has ruled in 2025, and it could continue for a while. Although volatility has a negative connotation, it can also bring opportunity. Therefore, we would like to reiterate our mantra of “proceed with caution” over the coming months.

2025 continues to be a year of change for the U.S. We monitor areas we feel are important to our clients’ financial situations and understand that the current changes are bringing uncertainty and increased market volatility. We are here for our clients should they feel apprehensive about their portfolio and financial plans.

We stay apprised of any changes to our clients’ personal situations such as divorce, health issues, selling of property, or any changes to their risk tolerance or time horizon. Additionally, we always recommend discussing any changes, concerns, or ideas they may have with us before making any financial decisions. Keep in mind that there are often other factors to consider when altering anything in your financial plan, such as tax implications. The more knowledge we have about their unique financial situation the better equipped we will be to best advise them.

Our goal is to exceed our clients’ expectations. We take pride in offering a high-level service that includes consistent and meaningful communication throughout the year.

Our team is here to help clients with every step of their journey toward their financial goals. Please feel free to reach out to us if you would like to explore our services.

We are accepting new clients!

Do you feel your advisor is fully aware of your financial situation?

- Yes No Not Sure

Are you satisfied with how your advisor is keeping you updated?

- Yes No Not Sure

Has your advisor reviewed your tax forms to understand how to coordinate your investments with your taxes?

- Yes No Not Sure

Has your advisor discussed tax planning strategies that could help you keep more of what you make?

- Yes No Not Sure

Is your advisor updated and current on tax planning strategies?

- Yes No Not Sure

Would you like a complimentary review of your financial situation?

- Yes No Not Sure

If you answered No or Not Sure to any of these questions, we would like to offer you a complimentary, private consultation with one of our professionals at no cost or obligation to you.

To schedule your consultation, please call us at (714) 597-6510.

In the first week of July, Congress passed a new tax bill that will change financial planning for millions of Americans. Here are four items within this bill that could impact you:

- Currently lower tax brackets will remain. The Tax Cuts and Jobs Act (TCJA) income tax brackets were to sunset at the end of this year. These brackets are now permanent, saving millions of taxpayers from a tax increase.

- Higher standard deductions become permanent. The higher standard deduction becomes permanent and will increase to $15,750 for single filers,$23,625 for head of households, and $31,500 for married individuals filing jointly. Also, there are new additional standard deductions for taxpayers over the age of 65 (subject to phaseouts).

- State and local deduction (SALT) are raised from $10,000 to $40,000, with a 1% increase in the cap each year through 2029 before returning to the $10,000 limit for 2030. The deduction is reduced for higher-income taxpayers starts to phase out after $500,000 of income.

- The estate tax exemption was increased from $13.99 million to $15 million for individuals and from $27.98 to $30 million for those married filing jointly.

We will be addressing these points and the details behind them in future communications.

Upcoming Events

- ID Theft Prevention Webinar | Wed, Sep 3 at 6pm

- IVC Wednesday Retirement Classes | 9/10, 9/17 & 9/24 from 6:30pm to 9:15pm

- IVC Thursday Retirement Classes | 9/11, 9/18 & 9/25 from 6:30pm to 9:15pm

- IVC Saturday Retirement Classes | 9/13 & 9/20 from 8:30am to 1pm

- FAN Tuesday Retirement Classes | 9/16, 9/23 & 9/30 from 6:30pm to 9:15pm

- MV Saturday Retirement Classes | 9/20 & 9/27 from 8:30am to 1pm

- MV Wednesday Retirement Classes | 9/24, 10/1 & 10/8 from 6:30pm to 9:15pm

- FAN Saturday Retirement Classes | 10/11 & 10/18 from 8:30am to 1pm

- Property Inheritance Webinar | Wed, Oct 1 at 6pm

- Investments Webinar | Wed, Oct 8 at 6pm

- Social Security & Medicare Webinar | Wed, Oct 15 at 6pm

- Understanding Dementia & Alzheimer's Disease Webinar | Wed, Oct 22 at 6pm

- Tax Update Webinar | Wed, Oct 29 at 6pm

- FAN Plan Basic Training Webinar | Wed, Dec3 at 6pm

Financial Advisors Network, Inc. is a registered investment advisory firm. The views stated in this letter are not necessarily the opinion of Financial Advisors Network, Inc., and should not be construed, directly or indirectly, as an offer to buy or sell any securities mentioned herein. Investors should be aware that there are risks inherent in all investments, such as fluctuations in investment principal. With any investment vehicle, past performance is not a guarantee of future results. Material discussed herewith is meant for general illustration and/or informational purposes only, please note that individual situations can vary. Therefore, the information should be relied upon when coordinated with individual professional advice. This material contains forward-looking statements and projections. There are no guarantees that these results will be achieved. All indices referenced are unmanaged and cannot be invested into directly. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment. There is an inverse relationship between interest rate movements and bond prices. Generally, when interest rates rise, bond prices fall and when interest rates fall, bond prices generally rise. There is no guarantee that a diversified portfolio will enhance overall returns out outperform a non-diversified portfolio. Diversification does not protect against market risk.

The S&P 500 is an unmanaged index of 500 widely held stocks that is general considered representative of the U.S. Stock market. The modern design of the S&P 500 stock index was first launched in 1957.Performance prior to 1957 incorporates the performance of the predecessor index, the S&P 90. Dow Jones Industrial Average (DJIA), commonly known as “The Dow” is an index representing 30 stocks of companies maintained and reviewed by the editors of the Wall Street Journal. Past performance is no guarantee of future results. CDs are FDIC Insured and offer a fixed rate of return if held to maturity. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed.

Sources: cnbc.com; barrons.com; bigcharts.com; reuters.com; thestreet.com; Federal Reserve Press Release; nerdwallet.com; cnbc.com; fortune.com; marketwatch.com; cnn.com; U.S. Department of Treasury. Contents provided by the Academy of Preferred Financial Advisors, 2025.

Turn Bulletins into Action

Stay informed—then come in for a free consultation and see how the updates apply to your financial life.