1st Quarter 2026 Newsletter

Entering 2026, almost every analyst forecasted that equity markets would experience a rise throughout the year. Will they be right?

Fueled by the optimism that characterized 2025, in late January of 2026, the S&P 500 reached new highs, and in early February the Dow Jones Industrial Average (DJIA) hit a record high, closing above the 50,000 mark for the first time. These moves were supported by expectations of interest rate cuts, continued earnings growth and improving economic and market trends.

As the quarter progressed, the favorable backdrop began to shift from momentum to volatility. By mid-quarter, rising geopolitical tensions, particularly in the Middle East, introduced a new wave of uncertainty. At the same time, evolving expectations around the Federal Reserve’s policy path added to investor concern. Together, these factors reignited volatility, marking a departure from the relatively smooth market environment investors had grown accustomed to.

March was a rough month for equities as indexes suffered significant declines. Although the S&P 500 staged a strong rally in the final days of the quarter, it was not enough to fully recover the losses incurred earlier in the month. The S&P 500 closed the quarter at 6,539 and despite its late rally, was down approximately 4.6% for the quarter. The Dow Jones Industrial Average closed the quarter at 46,254, and even after its end of month rally, finished the quarter down about 4.2%. These finished numbers were a reflection of a volatile quarter. (Source: Morningstar.com; cnbc.com)

Federal Funds rates were unchanged in the first quarter. As we know, Wall Street can respond significantly to any changes in monetary policy, but equities remained unscathed by the Fed’s decision to keep rates the same.

AI continued to be a strong influencer and Goldman Sachs Chief U.S. Equity Strategist Ben Snider forecasts that, "AI investments and AI cloud services will account for 40% for the S&P 500’s EPS growth in 2026,” as cited in Barron’s Magazine on March 19. That’s up from 25% in 2025. (Source: Barron’s, March 19, 2026).

Corporate earnings remained strong, with many S&P 500 companies expected to deliver roughly 12% to 13% year-over-year profit growth, marking the sixth consecutive quarter of double-digit gains. Growth was driven by continued confidence in artificial intelligence and a surge in energy-related profits due to higher oil prices. Performance varied significantly across sectors, with energy and industrial companies outperforming while a lot of technology and consumer sectors lagged. (Source: Marketwatch.com; 3/27/26)

According to the U.S. Bureau of Labor Statistics, the unemployment rate for February 2026 was 4.4%, holding relatively steady from January.

The energy sector was a constant in almost all headlines as oil prices soared during the quarter due to conflicts in Iran. The uncertainty around this conflict was a contributing player in the continued instability in equities.

While March’s volatility may serve as an early signal of a challenging environment ahead, the good news is after a rough quarter, markets did not experience a sharp correction like the one last seen in the first half of 2025. With all of this being said, the current market environment can be summarized in two words: Volatility persists.

Please remember, volatility is an expected part of the investment experience. Also, it should not be construed as entirely negative, as it can allow for good opportunities. As always, investors need to carefully choose portfolios that represent their unique objectives. As conditions evolve, maintaining a disciplined and well-structured investment approach remains essential. Our role as financial professionals is to closely monitor market developments and ensure your portfolio remains aligned with your time horizon, risk tolerance, and financial objectives. We remain committed to keeping you informed and well-positioned to navigate evolving market conditions with confidence.

Inflation & Interest Rates

Key Points

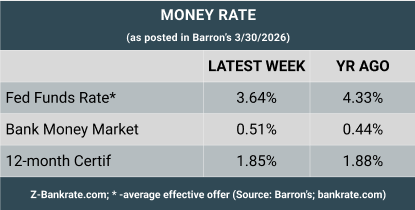

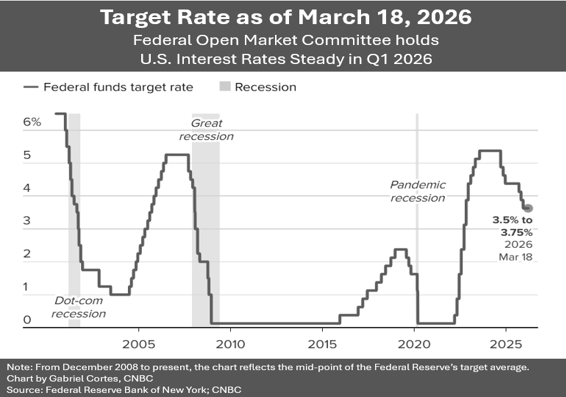

- Federal funds rates remained unchanged in the first quarter of 2026. The benchmark federal funds target rate range remains at 3.5 - 3.75%.

- The direction of inflation remains a concern, with added strain coming from oil prices.

- The economy remained strong despite potential drawbacks.

Through their first two sessions of 2026, the Federal Open Market Committee (FOMC) kept their benchmark federal funds target rate range at 3.5 - 3.75%. After enjoying three rate cuts in the last half of 2025, interest rates remained unchanged in the first quarter of this year.

During the March FOMC meeting, the committee also adjusted some previous views on the economy, notably, a slightly faster pace of growth and higher inflation projections for the remainder of 2026. Despite the elevated forecast for inflation, the Fed noted during this meeting that they still anticipate the possibility of future rate cuts.

The U.S. economy has remained remarkably resilient. Labor markets once again continued to show strength, and consumer spending remained healthy. This played into the Fed’s decision to hold rates steady.

Looking ahead, the Fed anticipates there could be additional rate cuts, however, the timing and magnitude are unclear, and they are, of course, not guaranteed. Interest rate movements will continue to be based upon the trajectory of inflation, labor market conditions, and the overall health of the economy.

In addition, how the conflict in Iran will affect the U.S. economy is “uncertain” according to the FOMC’s statement following the March meeting. Chair Jerome Powell shared during the subsequent press conference that it was, “too soon to know,” and continued that for the near term, measures of inflation expectations did rise due to the “substantial rise in oil prices caused by the supply disruptions in the Middle East.”

February’s Bureau of Labor Statistics data for the year-over-year core Consumer Price Index (less food and energy) rose as expected at 2.4%. Food prices were up 3.1% from a year ago and the price of shelter, which is the single largest component of CPI, posted a 3% annual gain (cnbc.com; 3/11/26).

Movements in interest and inflation rates are critical for investors' financial planning, and we will continue to closely monitor these key economic indicators.

The Bond Market & Treasury Yields

Key Points

- U.S. Treasuries experienced notable volatility in Q1 2026, with longer-duration bonds declining while shorter-term bonds provided relative stability.

- Amid persistent inflation and interest rate uncertainty, the yield curve continued to modestly steepen.

The first quarter of 2026 delivered a mixed environment for fixed income investors, particularly within U.S. Treasuries. While the year began with modest optimism and some early gains, the quarter ultimately turned negative for many segments of the bond market, especially longer-duration treasuries.

At the core of this volatility was the continued sensitivity of bond markets to interest rate expectations and inflation trends. Although the Federal Reserve did not implement any rate cuts during the first quarter, it suggested that rate cuts remain possible later in 2026.

In basic terms, bond prices move inversely to yields, so when yields rise, bond prices fall, and vice versa. During the first quarter, several factors contributed to upward pressure on yields, including:

- Renewed inflation concerns, largely driven by rising oil prices and geopolitical tensions,

- Continued economic strength,

- The Federal Reserve holding policy rates steady.

These dynamics impacted longer-term Treasuries, which are more sensitive to changes in interest rates.

As the quarter ended, the 10-year Treasury yield rose to 4.35%, the 5-year Treasury was 3.97% and the 30-year treasury was 4.91%. (Source: treasury.gov resource center)

For investors, bonds continue to play a meaningful role in portfolio diversification. While recent volatility highlights that bonds are not risk-free, especially in a rising yield environment, they can still provide relative stability compared to equities during periods of market stress.

As always, bond investments should be evaluated within the context of an investor’s risk tolerance, time horizon, and overall financial objectives. Bonds remain a core component of many well-balanced portfolios, and we will continue to monitor developments in inflation, Federal Reserve policy, and Treasury markets as conditions evolve.

Oil

.png)

Key Points

- U.S. oil prices, as measured by futures contracts for May deliveries of West Texas Intermediate, rose 77% to $101.38 for the quarter (Barron’s 3/31/26).

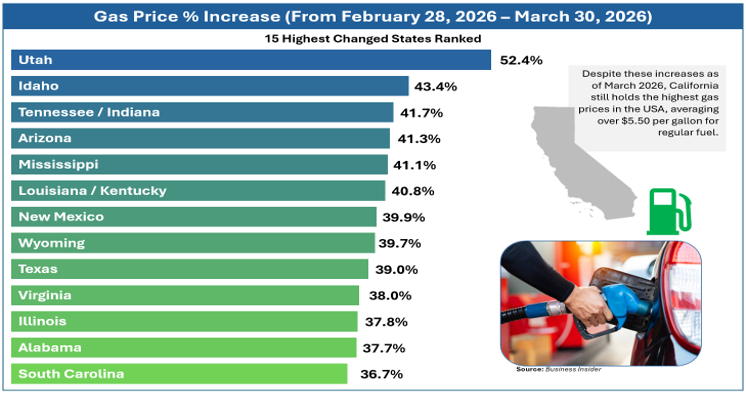

- The national U.S. average price for one gallon of regular unleaded gasoline ended the quarter at $4.02, the highest level since June 2022 (Barron’s 3/31/26).

Oil prices ended the quarter at levels not seen since 2022. Rising energy prices are a concerning factor for both businesses and consumers. The ongoing fighting in the Middle East has led to the closing of the Strait of Hormuz, which typically sees about 20% of the world’s oil supply flow through it.

While it is still too early to predict the full impact on economic growth, a lengthy continuation of highly elevated oil prices cannot be underestimated. Kristen Dougherty, Fidelity’s Energy analyst feels “in the longer term, the global oil market remains deep and liquid”, however, investors still need to be mindful of developments in the Middle East and their impacts on markets. Obviously, oil and energy prices are an area we are monitoring carefully.

Investor's Outlook

Key Points

- While we ended the quarter without reaching “correction” territory, volatility is likely to persist, making discipline and perspective essential.

- Maintaining a long-term focus and avoiding short-term distractions has historically been one of the most reliable ways to pursue financial goals.

Looking forward, the trajectory of equities in 2026 will likely depend on several variables, including the path of inflation and interest rates, corporate earnings, stability in the energy sector and of course the turmoil in Iran.

Geopolitical Conflict: The geopolitical conflict in the Middle East, particularly the war in Iran and its impact on global oil markets, took center stage in the first quarter and could continue to shape how market conditions move forward in Q2 and beyond. Any escalation or de-escalation could trigger reactive moves across equities, commodities, and currencies. The quarter closed with some optimism around a possible end or easing of geopolitical tensions, however, we need to keep a close eye on this matter.

Interest Rates and Inflation: As always, Federal Reserve policy remains a central influence. Any changes in the timing or magnitude of rate cuts could significantly impact market direction. While cuts are still anticipated, we may experience a “higher for longer” stance from the FOMC.

Corporate Earnings: Let’s also not forget about AI and its impact. According to Goldman Sachs Chief U.S. Equity Strategist Ben Snider, the “biggest current question for U.S. equity investors” is whether the significant investment in AI will ultimately translate into meaningful revenue and earnings growth (Barron’s, March 19, 2026).

While there is currently a high degree of volatility and short-term uncertainty, for the long-term, we remain positive. Moving forward, the media might continue repeating many words that could raise fear and concern, such as “dip”, “correction”, and “bear market”. Please remember, volatility is part of the investment experience and long-term investors know that the upward climb is never a straight line. A long-term mindset can help shield you from succumbing to media pressures and swaying from your financial goals and plans.

As you navigate through the next few months, please keep in mind that, as you can see from our chart, in an over seventy-year span, the S&P 500 has experienced a dip about twice per year; a correction about once every 18 months; and a dip of 20% or more once every six years.

Volatility can also present potential opportunities. Periods of market weakness can bring the ability to invest at more attractive prices, rebalance portfolios, or harvest losses to help offset capital gains.

We believe an informed client is the best client. Our commitment is to exceed our client’s expectations by delivering exceptional service, maintaining consistent, meaningful communication throughout the year, and proactively planning to help them navigate the changing economic environment. We keep our clients informed about developments that could impact their personal situation.

If you would like to explore our services, please contact us. We always recommend discussing any potential changes, concerns, or ideas that you may have with a qualified financial professional prior to making any financial decisions so they can help you determine your best strategy and make sure your plan is still aligned with your goals.

.png)

We are accepting new clients!

- Do you feel your advisor is fully aware of your financial situation?

- Are you satisfied with how your advisor is keeping you updated?

- Has your advisor reviewed your tax forms to understand how to coordinate your investment with your taxes?

- Has your advisor discussed tax planning strategies that could help you keep more of what you make?

- Is your advisor updated and current on tax planning strategies?

- Would you like a complimentary review of your financial situation?

If you answered No or Not Sure to any of these questions, we would like to offer you a complimentary, private consultation with one of our professionals at no cost or obligation to you. To schedule your financial consultation, please call us at (714 ) 597-6510 or email info@fanwmg.com.

Financial Advisors Network, Inc. is a registered investment advisory firm. Note: The views stated in this letter are not necessarily the opinion of Financial Advisors Network, Inc., and should not be construed, directly or indirectly, as an offer to buy or sell any securities mentioned herein. Investors should be aware that there are risks inherent in all investments, such as fluctuations in investment principle. With any investment vehicle, past performance is not a guarantee of future results. Material discussed herewith is meant for general illustration and/or informational purposes only, please note that individual situations can vary. Therefore, the information should be relied upon when coordinated with individual professional advice. This material contains forward-looking statements and projections. There are no guarantees that these results will be achieved. All indices referenced are unmanaged and cannot be invested into directly. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment. There is an inverse relationship between interest rate movements and bond prices. Generally, when interest rates rise, bond prices fall and when interest rates fall, bond prices generally rise. There is no guarantee that a diversified portfolio will enhance overall returns outperform a non-diversified portfolio. Diversification does not protect against market risk.

The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. Stock market. The modern design of the S&P 500 stock index was first launched in 1957. Performance prior to 1957 incorporates the performance of the predecessor index, the S&P 90. Dow Jones Industrial Average (DJIA), commonly known as “The Dow” is an index representing 30 stocks of companies maintained and reviewed by the editors of the Wall Street Journal. Past performance is no guarantee of future results. CDs are FDIC Insured and offer a fixed rate of return if held to maturity. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Sources: Barron’s; Business Insider; marketwatch.com; cnbc.com; Morningstar; U.S. Department of Treasury. Contents provided by the Academy of Preferred Financial Advisors, 2026

Turn Bulletins into Action

Stay informed—then come in for a free consultation and see how the updates apply to your financial life.